What do you think about when you encounter the phrase “swing trade.” Buy at the bottom of a stock’s trading range and then sell at the top. Yeah, right. Who doesn’t want to do that! Often, though, such aspirations translate to fanciful daydreaming, especially when one tries to confuse it for day-trading. Actually, though, the unflattering stereotypes combined with unyielding commitment to sound financial principles combine to make the recently-introduced Chaikin Analytics Bullish Swing Trade Screen a candidate for becoming my new favorite source of new ideas.

© Can Stock Photo / 8vfanC

The Bullish Swing Trade Screen

Recently introduced as a “starter screen” on Chaikin Analytics, the screen begins by identifying stocks within a Russell-3000-like universe that is rated Bullish or Very Bullish under the Chaikin Power Gauge model. That’s just one item, but it covers a lot of territory, including classic fundamentals such as Return on Equity, Debt, Earnings growth and consistency, industry strength, and Valuation. (Click here for more on the rank factors.)

Using this as a starting point immediately removes the screen from the realm of the fanciful and plants it squarely where we want to be, in the world of good financial fundamental sense. It allows us to assume that any stocks with good technicals, as defined in the screen, has them for sound legitimate reasons. Put another way, the screen stands squarely in the “technamental” camp.

Here are the remaining screening rules:

- The stock must exhibit three months’ worth of persistently high Money Flow: This refers to the Chaikin Money Flow indicator, which combines price movements and volume to indicate trends in demand and supply, or put another way, whether buyers or sellers are more motivated. Positive readings tell us that the market’s large participants (the ones who put the most money to work) like the stock.

- The Relative Strength indicator must be very strong: This is like saying the stock has a “bullish personality.” It isn’t complicated. It’s based on comparisons of the stock to the S&P 500. It depends, though, on the notion that stocks don’t persistently outperform or underperform the market at random. There’s a lot of fundament judgment inside this seemingly simple metric.

- The stock must be Oversold: This is what accounts for the “swing” in the swing trade. Surely you’ve noticed that no matter how consistent a stock is from day-to-day, it’s trend is never completely smooth. Trends are really combinations of many alternating up and down intervals. Sometimes the intervals are prolonged, other times they are brief. Sometimes the swings are relatively gentle, other times, they look wild. As with other market phenomenon, these happen for reasons. We may not always be able to explicitly identify the reason(s). Even so, reasons are there. One sample set of circumstances that might produce an oversold condition within a bullish trend is the completion or winding down by investors (institutional for example) of buying programs; many institutions establish or exit positions gradually over time to avoid disrupting the market and getting less favorable prices. Such reductions in buying activity, not because anyone has soured on the stock but simply because a big investor that wanted in finished the process of getting in, can in and of itself result in a temporary softening of the price. Beyond that, someone who was already in sees the new temporary peak as an opportunity to take profits (not necessarily because that investor has turned bearish; it may simply be a matter of cashing out of a winner to reallocate funds to something else). The same dynamic holds even if a different institution got in at a higher price sees the temporary peak as an opportunity to lighten up or exit. (It takes two to make a market, so we look for the weight of market opinion, not unanimity, which never exists). There are many ways to measure degrees of overbought or oversold. One popular indicator is the Welles Wilder RSI. This screen uses a proprietary Chaikin formulation.

- The stock’s Beta must be between 1.00 and 2.00: When we see a stock that is significantly oversold, there are two things we, as potential buyers, would not appreciate. First off, we would not want so see what we think of as an oversold “barrier” off of which we expect the stock to bounce wind up being the first rest stop in what ultimately turns out to be a new and prolonged downward journey. The other screening factors help us to assume the former rather than the latter. But having a Beta no higher than 2, meaning the stock is not usually two or more times as volatile as the market, serves as another source of support. The other thing we don’t want is for the stock to stay where it is or bounce only a trivial amount. A Beta of at least 1, meaning the stock has not been habitually less volatile than the market, helps us in this regard.

- The stock price must be at least $10: This steers the result-set away from names that are likely to be less liquid and/or less appealing to institutions.

Evaluating the Screen

The usefulness of a screen is determined by the extent to which it helps you identify stocks worthy of being evaluated. We’re looking for a small personal (designer) stock market that is carved out of the larger market. This personal stock market should be limited to a manageable (analyzable) number of stocks all of which conform to your investment goals, and a successful screen is designed such that the probability of identifying winners is greater than it is for the market as a whole.

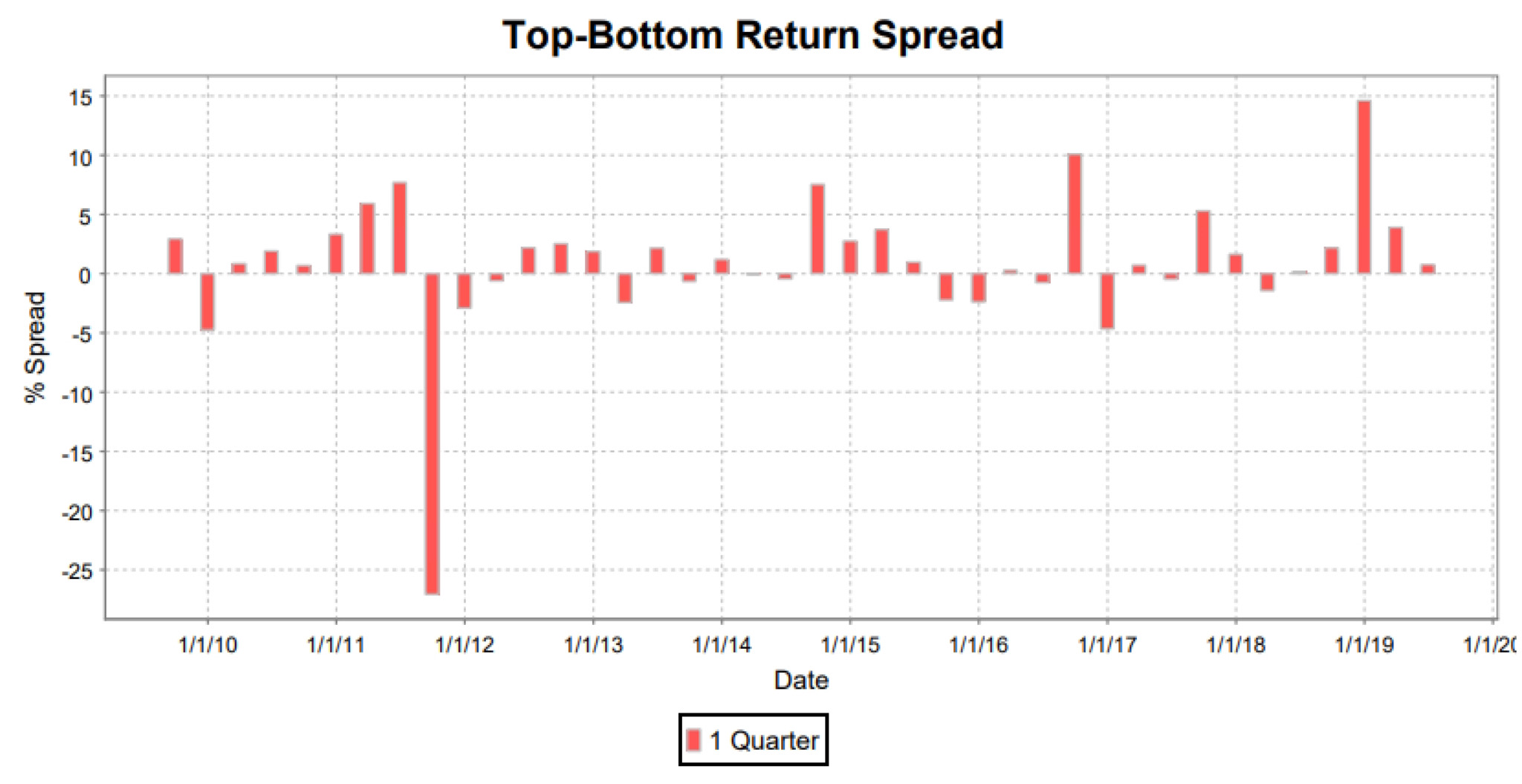

Figure 1 shows the quarterly difference in the average return of Russell 3000 stocks that appear in the screen versus the much, much larger group of Russell 3000 stocks that do not appear.

Figure 1 – Quarterly

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

As seen, and as discussed when the image was introduced last week, notwithstanding the quarter from hell in 2011 (when the market was being plagued by such unfortunate oddities as the Arab Spring, and the Greece-Euro crisis), you would have been better off making choices from the limited, personal screen-created stock market than from the much-bigger general market.

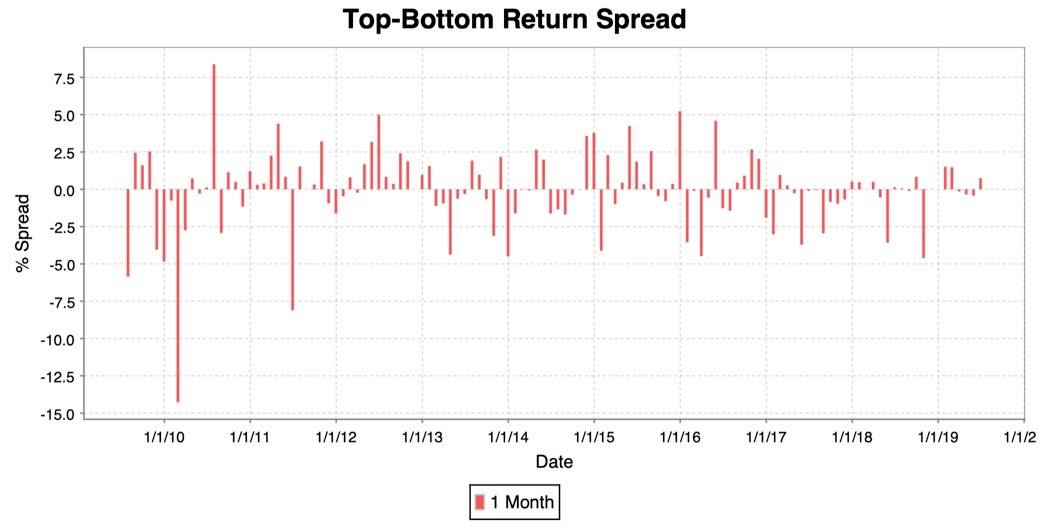

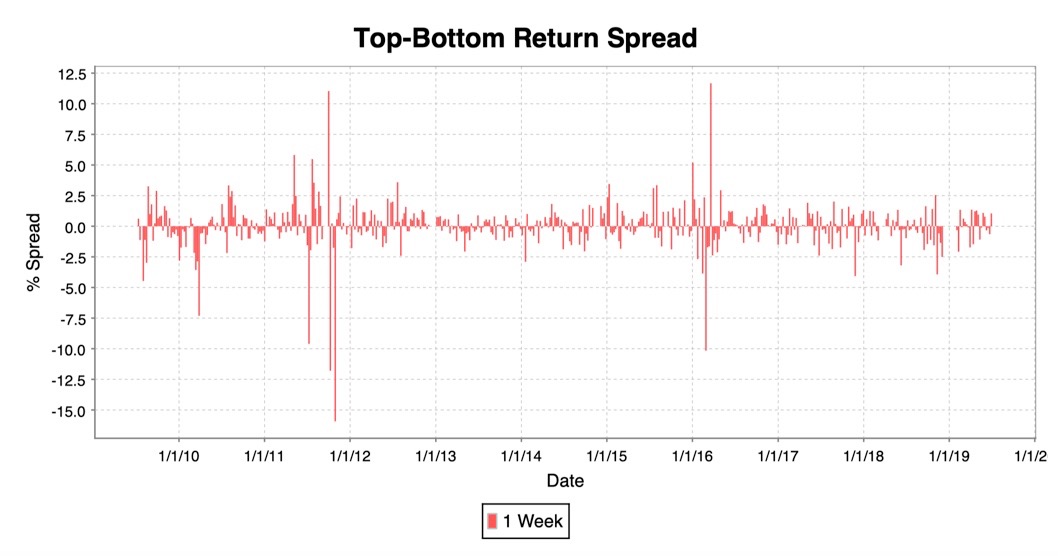

That assumes quarterly holding periods. To many, that might seem like a long time for a screen whose name includes the phrase “swing trade.” Figures 2 and 3 show what the spreads would have been had we used monthly or weekly hold periods respectively.

Figure 2 – Monthly

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

Figure 3 – Weekly

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

Whenever any strategy has the “word” trade in its title, it’s tempting to assume one has to move quickly, to act on the latest information as quickly as possible. Although vendors of hardware to enable super-high-speed trading might not want to hear it, high speed may not be all its cracked up to be. Data may move in nano-seconds, but humans still move at human speed and ultimately, businesses and customers consist of humans. So to me, it comes as no surprise to see that the efficacy of the screen improved as the assumed holding period stretched. Stories need time to develop and get reflected in stock prices.

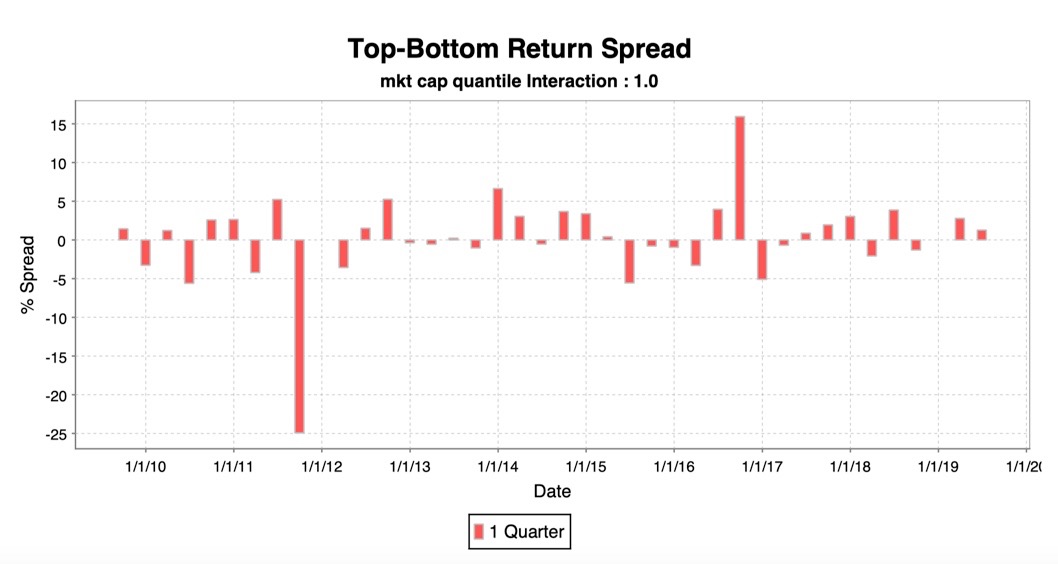

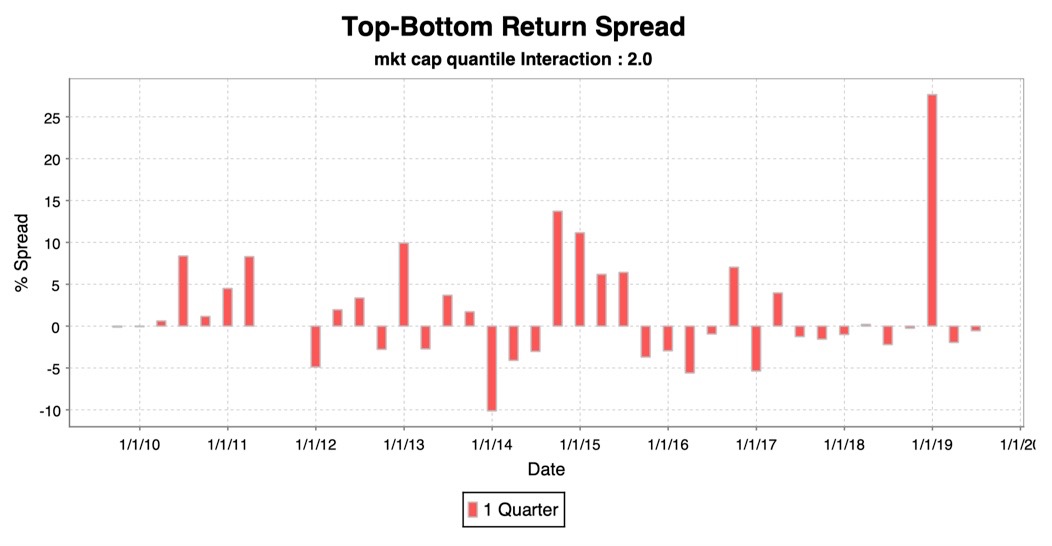

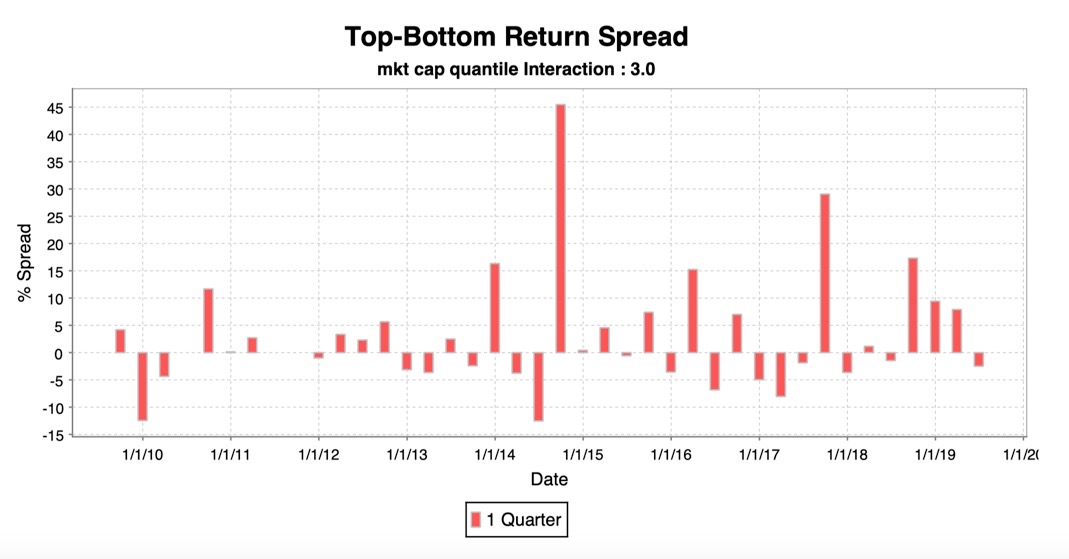

Figures 4, 5 and 6 break the test down into subsets of the Russell 3000; the top-third (in terms of market cap), the middle third, and the bottom third respectively.

Figure 4 – Quarterly – Largest subset of Russell 3000

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

Figure 5 – Quarterly – Middle subset of Russell 3000

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

Figure 6 – Quarterly – Smallest subset of Russell 3000

Image from ClariFi, a subsidiary of S&P Global Market Intelligence

Many who are experienced in screening and other forms of quant work often notice that their models tend to be more successful among smaller stocks. Some of this is attributable to test periods that include times when small-cap stocks were stronger in general. But even beyond that, it often seems that the large followings and exceptional availability of information about large-caps make market inefficiencies harder to identify and exploit. This screen seems noteworthy in that it has shown efficacy at all ranges of sizes, although the mid- and smaller- sized subsets seem to hold better potential for home runs.

The Passing Stocks

When the screen was run on 7/22/19, the following stocks made the grade:

Arconic (ARNC)

Axalta Coat Sys (AXTA)

Bruker Corp. (BRKR)

Esco Tech (ESE)

Fleetcor Tech (FLT) *****

Foster Lb (FSTR)

Hexcel (HXL)

Innospec (IOSP) *****

John Bean Tech (JBT)

Laboratory Corp (LH) *****

Lantheus Holdings (LNTH)

Natera Inc. (NTRA)

Powell Inds. (POWL) *****

Vectrus (VEC)

***** These stocks also exhibited “Oversold Buy” signals under a separate Chaikin algorithm.

7 thoughts