In the eyes of many, Book Value (BV), the metric traditionally favored by academicians as an anchor for the much revered albeit-lately-poorly-performing value factor, was sort-of pronounced dead on February 23, 2019. That’s the date of the latest Berkshire Hathaway (BRK.B) annual shareholder’s letter in which Warren Buffett, perhaps BV’s number-one non-academic fan stated, with respect to this year’s letter’s having departed from its long-standing tradition of opening with a statement of the change in the Berkshire’s BV: “It’s now time to abandon that practice.” As if to pile on, Buffett next stated “that the annual change in Berkshire’s book value – which makes its farewell appearance on page 2 – is a metric that has lost the relevance it once had.” That strikes me as a call to action — to defend book value! (I suppose it’s in character; I’m the guy who, at a writing workshop I used to attend responded to the multitude of fantastical dystopian submissions I’d been seeing by suggesting that I was might try to drum up a class action lawsuit challenging discrimination against zombies.)

© Can Stock Photo / Woolwerth

Putting On My Old Lawyer’s Hat

Personally, BV is not by any means my favorite valuation yardstick. I’ve tended to favor Price-to-Sales, Enterprise Value-to-Sales, Price-to-Estimated Earnings, and with a dash of comparisons to free cash flow (but not overdoing it because FCF can get very volatile and because accruals — another despised and discriminated-against metric — actually tells us more than many realize). I did include Price to Book Value (PB) in the pre-built “Basic: Value” ranking system I built for portfolio123.com but that wasn’t so much a matter of conviction but a sense that it ought to be there given my intent to create a fairly generic system users could edit if and as they wished.

Buffett’s letter did a number on my head. Should I revise that pre-built ranking system? Should I consider ceasing to use that ranking system in a separate large-scale factor-related project on which I’m working? That mental stalemate (along with another just-completed rush project) is why I hardly published anything in over a month.

But then, I remembered debates I used to have with George S. Meissner, who gave me my first law job, about defending people who absolutely-positively did it (which was pretty much the case for every one of our criminal defense clients). Everybody is entitled to have their rights asserted, he said. Even the guilty are at least entitled to make the prosecution go through the burden of proving guilt beyond a reasonable doubt under proper procedures and with properly admissible evidence. “What would you do if you were accused of a crime? Wouldn’t you appreciate that?” he asked. My answer: “I’d just hire you.”

Ultimately, though, he was right. Everybody is entitled to a defense; corrupt nursing home operators, killers . . . and of course zombies, and yes, even Book Value.

What, Exactly, Is Book Value

An accountant would explain that this is the the purchase price of an asset, minus adjustments such as depreciation and amortization (fancy calculations that supposedly incorporate the deteriorating usefulness of that asset as time passes) plus adjustments for amounts you spend to improve the asset over the course of its life. Things then get complicated because accountants think in terms of double entry, which means we can’t ignore money used to purchase (and possibly improve) the asset . . . .

Wake up, it’s not all that bad.

When we switch to the investor’s vantage point, we typically talk about the company as a whole, not each individual piece of it. Now, book value is the amount of “permanent” capital attributable to owners of the business (i.e., the shareholders), as opposed to creditors. (Non-permanent capital, formally referred to as “current,” means money the company money or other assets that is expected to depart quickly — in less than a year — as part of the ordinary day-to-day operations of the business, such as inventory that gets sold or money that will given to employees when paydays arrive, money that will be given to suppliers for all the stuff that was bought other than C.O.D., etc.).

Book Value and Intrinsic Value or Market Value

Now things get interesting.

In theory, book value is the value that should be received if a company is sold.

That’s pretty much the case when we sell a car. We expect to get, or at least the buyer expects to pay (forget what sellers expect, they always start with big dreams) the initial price of the car minus whatever amount the buyer can bludgeon the seller into accepting as compensation for wear and tear, plus the value of any new goodies being included, such as, perhaps, new tires that were added just last week.

It should be the same for a company; the price paid for the assets, less wear and tear plus the value of improvements. So logically, it might seem that the price of a publicly traded stock should be equal to its book value per share.

In the real world, it almost never works this way. In fact, among the 6,549 stocks in the Portfolio123 US Fundamentals Universe as of this writing (the really big universe that even includes lots of virtually un-tradable penny stocks) the number trading at a Price-to-Book Value (P/B) ratio of 1.00 was, exactly, zero. Adding a 5% margin of error above and below 1.00 produced only 227 stocks, a mere 3.5% of the universe. Among S&P 500 constituents, we find only 6 (1.2% of the total) within a 5% margin for error.

Then again, this is the same situation we face with any attempt to measure a stock’s true or intrinsic value. In theory, we know exactly how to do it. Intrinsic value is the present value of all future cash flows one expects to receive as a result of owning the asset. In reality, it’s incredibly hard to calculate since we’re talking about the future; we cannot precisely estimate future cash flows, nor the timing of these cash flows.

So when Warren Buffett says, as he does, “it is likely that – over time – Berkshire will be a significant repurchaser of its shares, transactions that will take place at prices above book value but below our estimate of intrinsic value” you should mentally add the following: “Book value is a conservative single point in time ‘snapshot’ of a company’s value that makes no allowance for future growth and profitability. Our expectations of the future are such that buying back stock at a premium to book value will be fine so long as we buy at a discount to our expectations of book value plus the impact of future growth and profitability.”

But what about intangibles, all the great things that book value supposedly does not take into account?

© Can Stock Photo / dizanna

Actually, book value take more into account than critics realize. Suppose I own a brand (I’ve registered all the intellectual property that needs to be registered) You want to buy it from me. How will you determine how much you’ll pay. Don’t even think of saying “I’ll pay the value of the brand” because if you do, you can bet I’ll pull a number out of my gut that’s well into the hundreds of billions. How will you argue me down? The answer: You’ll go through some sort of mental gymnastics that will, at the end of the day, get you to something that resembles an estimate of the present value of how much you can earn as a result of owning the brand. We’ll bicker over the details (especially if you counter my $450 billion offer with an ask somewhere around $1.5 million). We’ll shout. We’ll curse. We’ll each threaten to walk away from the deal several times. And we’ll consult with other people. Eventually, though we’ll come to terms — and assuming you went through something that’s at least vaguely analogous to a present-value-of-expected-cash-flows exercise, chances are the sale price will wind up a lot closer to $1.5 million than $450 billion (maybe, if you’re in a good mood, you’ll throw me a bone and we’ll do the deal at $1.8 million).

What about comparables? Why think of future cash flows when we can look at prices at which comparable assets recently sold. How do you think those were valued? Maybe that language wasn’t overtly used. But look at it this way. There are two kinds of comps: (1) Comps whose valuations were somehow or other related, however debatable the details may be, to the buyer’s expectations of future cash flows and timing, or (2) Comps that later come under the supervision of bankruptcy trustees. (I did junk bonds back in the ’80s. Believe me, I’m not kidding here.)

Bottom line; Whether it’s a dividend stock, a patent, a Treasury note, a copyright, a piece of real estate, whatever . . . somehow or other the value will have to be pegged (however imprecisely that my be given that we’re all imperfect humans dealing with the unknown future) to the present value of expected future cash flows.

Book value is a very conservative approach to this. It takes into account cash flows received in the past, if any, from intangibles — profits that are not paid out as dividends accumulate in an accounting entry known as “retained earnings” which is a part of the “common equity” section of the balance sheet, and in popular parlance, especially when discussed on a per-share basis, common equity is referred to as . . . you guessed it, book value.

So book value for a company does not ignore intangibles. Profits attributable to the intangibles, in the past, if any, find their way into book value via the retained earnings account. What about the future (an especially critical question if the intangible has not yet been monetized, such as a patent that has not yet been used as part of a commercial product)? What book value does ignore is future growth expectations That’s why we should never expect the P/B to always equal 1.00. Stocks trade at discounts to or premiums above book value based on future expectations — a familiar refrain from other aspects of stock valuation.

© Can Stock Photo / ileezhun

So when Warren Buffett says Berkshire’s intrinsic value is above its book value, that is not a statement of fact. It’s the expression his favorable opinion regarding Berkshire’s future. He’s also implicitly stating that future prospects are accelerating, that being why he thinks the stock should grow faster than observable growth in book value.

Book Value’s First Cousin – Return on Equity

While Buffett may seem to have dissed Book Value, I’m yet to hear him cast aspersions on Return on Equity (ROE), which is profit divided by equity, or put another way, profit divided by book value.

ROE is, indeed, very important to Buffett. We see that in so many words from Robert Hagstrom’s 1994 classic The Warren Buffett Way, which is based on Hagstrom’s interpretation of Buffett’s beliefs as expressed through the annual Berkshire shareholders’ letters. As to Hagstrom’s accuracy, all I can say is that back when I was covering Berkshire at Value Line, I asked Buffett straight out about the book. He told me he did not work with Hagstrom in any way but that he read the book after it was published and that he had no objection to any of its content. That was about as close to an endorsement as he was likely to give.

I’ve seen nothing from Buffett in the years since to suggest he has abandoned ROE. Indeed, Apple (AAPL), a tech company in which Berkshire is invested despite the old stereotype that Buffett was tech averse, has a 5-year average ROE of 40.6%. Not everything Berkshire owns or craves has super ROE today. For example, Buffett and Charlie Munger engaged in some self criticism for not having invested in Amazon (AMZN) or Alphabet (GOOGL), both of which have 5-year average ROEs that are ok (11.66% and 14.21% respectively) but which are trending up (respective trailing 12 months ROEs of 30.06% and 16.26%).

The growth angle is important. It’s the key to how P/B should be used.

Using P/B

I start valuation with the Gordon Dividend growth model, which says fair price is equal to future dividends divided by the difference between required rate of return and expected growth rate. Substituting Earnings for Dividends (something I feel comfortable doing given an investment-community culture that has long been willing to regard all earnings as belonging to shareholders (with them voluntarily choosing to allow management to reinvest some or even all of it in lieu of paying cash dividends), I get this:

P = E / (R – G) which, with some simple algebra, can be re-expressed as:

P/E = 1/(R – G)

Where,

P = price

E = Earnings

R = Required Rate of Return (which depends on the risk free rate, the risk premium one expects from holding risky equities, and a measure of company-specific risk)

G = expected future growth

This is not a formula for Excel. Some defy precise estimation (especially the idea of an infinite rate of growth). But it is a framework that helps us evaluate valuation ratios, showing, for example, that fair P/E rises as growth rises and/or as company-specific risk falls, and/or as market interest rates fall. For more details on this framework, click here.

Here’s how Book Value and P/B fit in.

E = B * ROE (earnings is equal to book value times return on book value, or return on equity).

Therefore, substituting B * ROE for E, we get:

P = (B * ROE) / (R – G)

With some algebraic reshuffling, we wind up with:

P/B = ROE / (R – G)

Again, none of this is to be taken literally as being plug-and-play. It’s a framework and an important one at that. It shows us that:

- Fair P/B should rise as ROE rises;

- Fair P/B should also rise as expected future G (growth of ROE) rises; and

- Fair P/B should rise as R falls (reductions in company-specific risk will cause R to rise thus exerting upward pressure on P/B all else being equal.

Making Sense of the BM (Book-to-Market) Value Factor

For some reason academicians, like to put book value in the numerator and express it as a company-wide rather than a per-share metric. I have no idea why (maybe they like the bathroom-oriented association with BM — if you don’t get it, skip it). Out of habit, I prefer to express it as P/B. Same thing. (Just understand that in academic papers, higher BM suggests better valuation; for me better valuation is implied by lower P/B.)

Does this really make sense as a “factor?” Absolutely not. It never did. It doesn’t now. And it never will. Neither P/B nor any other valuation metric can be assessed on its own. It always depends on other things; in the case of P/B, those other things are R, G and ROE.

That’s why studies of the BM (as they say it) factor seem to point to nowhere. Let’s take a little look at P/B when we use it properly, with reference to ROE and G (I’m going to stick with these, since these are more likely than not to loom as the deal breakers than will Required Rate of Return).

Testing P/B

Starting with a Portfolio123 universe built to approximate the Russell 3000, I set up a single factor ranking system for P/B. I set it up such that highly ranked stocks are better (i.e. have lower, seemingly “cheaper” P/B ratios). So if all goes well in my testing higher rated stocks should perform better.

© Can Stock Photo / yeyen

I screened based on three factors:

- The P/B rank (higher is better)

- The percentile rank of the 5-year average company ROE (higher is better)

- The score under the Portfolio123 “Basic: Growth” ranking system (this is a very, very, very crude proxy for expected future growth of ROE that consists of historical growth patterns for sales and EPS, which means I’m naively assuming the past will persist — something I’d be loath to do with real money)

I used Portfolio123’s rolling backtest protocol to do a test that won’t depend on the fortuitous choice of a single start date. On week one, I run a self-contained start-to-finish 13-week test. At the beginning of week two, I run another self-contained 13-week test. At the beginning of week three, I run another 13-week test. And so on and so forth. Then, I average the results of all of these 13-week tests and compare them with changes in the benchmark — I’m using the iShares Russell 3000 ETF (IWV) — over the same intervals, and then average the results. (By the way, all figures are adjusted to reflect dividends, meaning we’re looking at total return.)

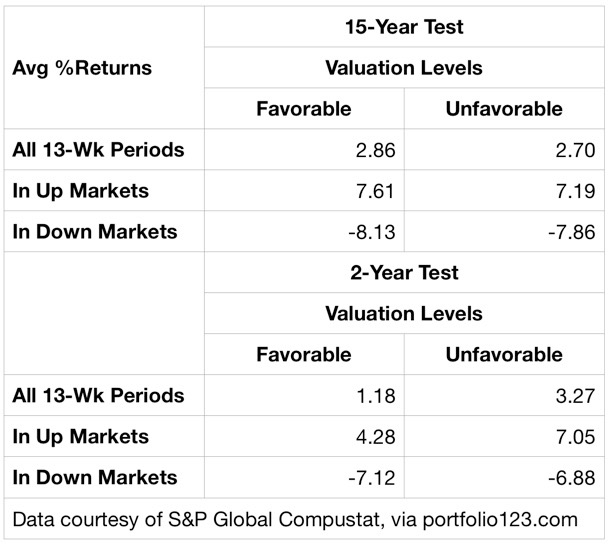

Table 1 starts us off by looking only at P/B and by doing so for the past 15 years and for the last two years, the latter as horrendous a period for just about any kind of value metric; i.e., the great value inversion (which may or may not be over). The Favorable Valuation group includes stocks whose P/B ratios ranked in the lowest 35% of the universe; the Unfavorable group refers to those whose P/B ratios were in the highest 35%.

Table 1

What we see in Table 1, a whole lot of nothing, lt would be disappoint many conventional and academically inclined value adherents. But for those who appreciate the above framework, the one that equates ideal P/B to ROE divided by the difference between required rate of return and growth, Table 1 is exactly on script. When we look at P/B is isolation, we should expect nothing, and nothing is what we get.

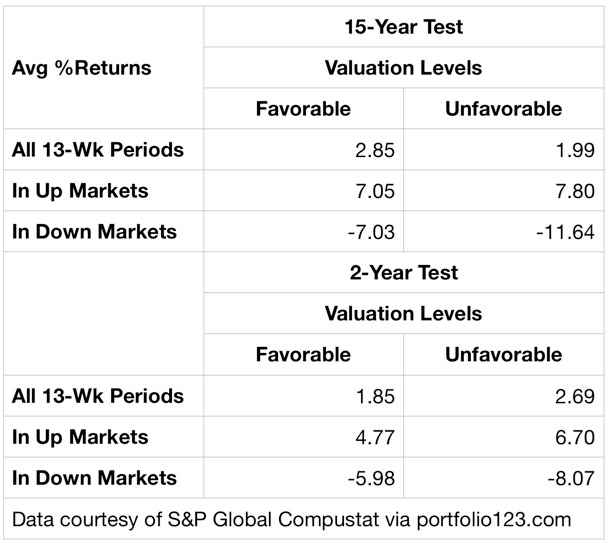

Table 2 shows what happens when we rank by P/B within a sub-universe that has been pre-qualified to address ROE and Growth (again, the latter having been crudely and naively estimated). For the Favorable versions of these screens, I started by limiting consideration to top 35% tallies for 5-year average ROE and the Portfolio123 “Basic: Growth” ranking system. Within this sub-universe, I accepted only stocks whose P/B ratios ranked in the lowest 20%. For the Unfavorable screens, I flipped the criteria; bottom 35% in terms of ROE and Growth and highest 20% in terms of P/B ratio.

Table 2

Now we’re seeing some things. Over the past two years, consistent with the great value inversion, we see that overall results for the Favorable group trailed those of the Unfavorable group. P/B is not by any means alone in this value-factor nightmare; if you know of a value factor that wasn’t a mess, please tell me — or better still (for you), don’t tell me: Keep it to yourself, trade the daylights out of it, and then go buy for yourself a tropical island or two.

But before weeping over the dark ages of value, check the last row of the table, the one that compares performance only during down periods. As crude as my growth rules was and as dismal as the period has been for value in general, low P/B, when used in conjunction with the factors it ought to be matched with, did well. It steered us away from stocks that on average did about 200 basis (not annualized) points worse per 13-week period.

Now go up the Table and check the longer-term 15-year track record, a period that includes the recent armageddon, the 2008 crash and recovery, and a lot more less-dramatic years. Now we see that P/B, again when used in conjunction with things we ought to be considering alongside of it, dd OK. The Favorable group outperformed the Unfavorable group by 86 basis points per 13-week period.

We also see that use of P/B, even within this broader range of environments, did not shine during up-market intervals. But it was a huge boon during down periods, enough so to have produced the better tally for the overall 15-year period.

Food For Thought

Notwithstanding Warren Buffet’s having closed the curtain on his shareholder-letter-leading-starring-role for book value, I believe the metric remains as relevant as ever. It’s a viable, albeit conservative, estimate of a company’s here-and-now intrinsic value assuming growth is zero. Any suggestion that intrinsic value is higher, whether due to the greatness of intangible assets or whatever, is and should be read as a statement regarding future growth (monetization) prospects.

In times when the market is optimistic and willing to pay up for future expected growth, the staunchly conservative P/B metric is not the metric of choice; unlike P/E, P/S, etc. But for less buoyant times, intervals during which investors are less inclined to chase growth stories, P/B, used correctly (i.e. with attention to ROE and growth) can be quite useful.

Looking at the world as it now is and as its been more often than not since Henry Kaufman (How many readers remember him?) issued his 8/82 proclamation that then-high-double-digit interest rates would start to plummet, conservative investment postures seem quaint, or even pitiful and Book Value would seem to belong on the scrap heap. But looking at things in perspective, now, with interest rates capable of significant moving that are only sideways or up but not meaningfully down, this may be the worst time imaginable to declare the death of book value and all that’s related to it (P/B, ROE, etc.).

PB-ROE works well when capital is the limited resource. This is true of many financials. But if sales is the limiting factor, you might want to look P/S-Profit Margins. More here:

https://alephblog.com/?s=PB-ROE&submit=Search

LikeLike