If you want to stand out from the investment-community crowd, you’re probably going to want to be in stocks/ETFs the crowd isn’t seeing or buying. Let’s face it, no advisor is going to attract new clients by loading up on the S&P 500 SPDR ETF (SPY). Venturesome equity investors often do this by aiming at small- or micro- or even nano-cap stocks, and (hopefully) understand the increased risk they’re taking on. In the ETF world, we can also aim small, but not too small (liquidity requirements limit how far down in size ETF portfolios can aim). Interestingly, though, the way ETFs are set up, we don’t have to sacrifice size, stability or even liquidity in our quest to avoid the crowd. We can find ETFs that are relatively hidden even within as conspicuous an areas as, say, large-cap value. And our quest for the obscure might even find some ETFs that do a better job interpreting “value” than do the biggest names.

© Can Stock Photo / Colour59

First Things First: Why Large-Cap Value — Now?

Value has been under a lot of pressure for a long time. But it’s not so much that the market hates low ratios (P/E, P/S, etc.). It’s been more a matter of Mr. Market’s long love affair with companies whose shares carry high metrics. High P/E is dangerous, not in and of itself, but only if or when the market comes to realize that the growth expectations (or dreams) that support high ratios are not going to be achieved. We saw it in the 1960s with the once-beloved “Nifty Fifty.” We saw it in the early 2000s with then-new internet stock. But we’ve lately come through a very long business expansion, accompanied by a new generation of newly introduced businesses, that for a long time have made disappointment, or unfulfilled expectations seem like a thing of the past. Hence many high-valuation equities had no reason to fall — so far.

There’s a lot we don’t know not just about the still-ongoing covid-economy and market, but also what the post-covid world will look like. And even without covid, interest rtes had already plunged to a point where they can not provide the sort of tailwind equities and the economy have enjoyed for most of the last 40 years. Expectations today are more likely to be disappointed than in many years. So don’t give up the ghost on value. Rather than considering it dead, it may be better to prepare for a possible reawakening following a long sleep.

As to large-cap, I could care less about the so-called Fama-French size factor. Size is a substantive measure of business risk, and at the time, I’d still like to hold the line on risk.

The Usual Large-Cap Value Suspects

Browsing on PortfolioWise for large-cap ETFs, I naturally saw offerings by all the big-gorillas in the ETF space: SPDR, Vanguard, Schwab, iShares, etc. They were all ranked Neutral under the PortfolioWise Power Rank system, and they all had names that suggested the same old thing; follow indexes that select stocks by ranking a bunch of large caps (to 500, top 200, top 1000, whatever) according to some of the standard ratios (P/E. P/B, P/S, etc.) and choose however many the fund creator wants. Add in a few specs covering portfolio weighting (often by some version of market cap), rebalance schedules, and the like, and voila, there we have it; yet another generic large cap value ETF.

Beyond The Usual

One ETF, on the list jumped up at me even though I never herd of it Xtrackers Russell 1000 US Quality at a Reasonable Price ETF (QARP) (ETF Home). It stood out as the only Bullishly ranked large-cap ETF in what was otherwise a sea of Neutrality.

Meanwhile, I recognize Russell 1000 and therefore understand this ETF is firmly planted in the large-cap camp. But Quality at a Reasonable Price? I know what Growth at a Reasonable Price is (good old GARP). But QARP; that’s different. Another eye-catcher: QARP’s Group Rank was near the top at 2 (out of 19).

So we have three easy-to-spot clues that we may be onto a non-generic potentially-interesting ETF: (i) a Bullish future-performance-oriented rank, (ii) a high Group rank, and (iii) a name that that inspires curiosity — in the ETF world, unlike in the stock market, “security” names can in and of themselves be important cues.

Red Flags?

QARP has only $84.4 million in AUM (Assets Under Management) and its trading volume averages only 40,000 shares per day.

© Can Stock Photo / britishpics

In the stock market, small size appeals to many investors when but when small is pushed so far as to cripple trading liquidity, that alone can blow up an investment even if the company if OK. But the ETF world is different. Here, whether the fund itself trades actively is not all that important. It’s about “creation units” and whether the securities in its portfolio trade actively (click here for more on this topic and how it played out recently in fixed income). QARP is a large-cap ETF and the securities it holds can all trade as easily as any in the stock market. So absent an oddball flash-crash of sorts (which can impact any security no matter how liquid it usually is), one who wants to buy or sell QARP can comfortably assume they’ll be able to do so at a price that’s in line with the net asset value of the portfolio.

Commercial risk, however, is real. Is QARP a profitable venture for the Xtrackers brand and DWS Group, the firm that owns it? DWS is under no obligation to keep QARP going, or even the Xtrackers family. It may not be critical that QARP be profitable in and of itself; DWS may or may not see it in terms of its role within a comprehensive Xtrackers family. But ultimately, any ETF can be terminated, and this is something that does actually happen, when sponsors determine funds are not commercially viable and not likely to become so in a reasonable time frame.

But here’s the “good” news. Termination of an ETF just means liquidation of the portfolio and distribution of proceeds to shareholders. This can get dicey for ETFs that own hard-to-trade assets. But for ETFs that own large-cap highly-liquid stocks, very prompt receipt of 100 cents on the dollar — right into the brokerage account, which will often label the transaction as if it were an ordinary sale— can be expected. The risks are not so much financial but matters of convenience and image (advisers who invested client proceeds in illiquid ETFs — without openly discussing the matter with clients— may wind up having some awkward conversations later on).

So a decision to invest in a tiny ETF should be made case by case with a view toward the liquidity of the underlying portfolio and a balance between the image/convenience risk versus the opportunity. Advisers, depending on the nature of their practice and clientele, may find clients impressed at the very least by the ability of the adviser to have such discussions and also by the opportunities themselves.

The Large-Cap Value ETFs I’m Considering

Tables 1a and 1b show the Large-Cap Value ETFs I found on Portfolio Wise that caught my attention. By way of comparison, the tables also show the two largest most well-known ETFs in the space; Vanguard Value (VTV) (ETF Home) and iShares S&P 500 Value (IVE) (ETF Home).

Table 1a

Table 1b

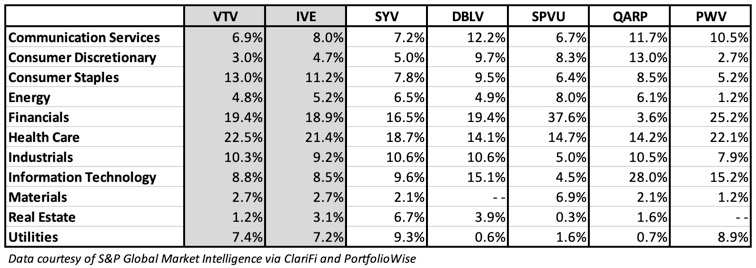

Table 2 shows the way each of these ETF portfolios are allocated among sectors.

Table 2

My Criteria For Choosing

I’ve long been bothered by the way Value is often implemented in the investment community — a naive quest for the lowest valuation ratios available. A first-grader — any human who can recognize one number as being lower than another — can do that.

Value is not about buying stocks priced cheaply (the value “factor”). It’s about buying stocks that are priced below the level at which they should be priced given the characteristics of the company being purchased (value “investing”). Click here for more on the difference. Skipping the intricacies, value investing is about finding stocks whose P/E, etc. are low relative to future growth prospects and or business risk/company quality. (Click here for the intricacies.)

© Can Stock Photo / webking

VTW and IVE, the two big gorillas in Tables 1a/1b differ in details but each, in their own way, aims for the value-factor, the approach I do not want. Ditto other big-name value ETFs. So I’m going to look at the others to see which, if any, comport with what I really want to achieve — value “investing.” The Group Ranks will serve as worthy quant feedback and recent performance data will be interesting to see how the market in various historic periods as reacted to the ETF’s chosen strategy (recognizing that value in general has been treated badly by the market for quite a while.

Evaluating The Candidates

Invesco S&P 500 Enhanced Value ETF (SPVU) (ETF Home): This jumped right off th page because of the weak Group Rank. The name, which included the word “Enhanced,” encouraged me to expect good things. But it turns out the SPVU not only uses the plain value factor, it doubles down on it by weighting its positions not just on market cap (as many ETFs do) but on a combination of market cap and the value score. I’d like that if the score included some measures of growth and/or quality in order to have taken into account the reasonableness of the value ratios. But that’s not happening. I’m out.

Xtrackers Russell 1000 US Quality at a Reasonable Price ETF (QARP) (ETF Home): This Bullishly ranked ETF and its high Group Rank was my jumping off point for this exploration. And I like its strategy even more. Market cap weighting is the starting point. And as with SPVU, the capitalization weight is adjusted by a value score. But unlike SPVU, the weight is also adjusted by a quality score (which reflects profitability, efficiency, earnings quality and leverage). In fact, the quality score is multiplied by two! This is music to my ears. In a perfect world, I’d also want it to bake in a future-growth score but quants trend to struggle with future growth so I won’t bet greedy here. I’m in.

Invesco Dynamic Large Cap Value ETF (PWV) (ETF Home): Dynamic? That rings a bell. Way back in time, Invesco bought PowerShares, one of the earliest ETF companies to offer “dynamic” ETFs, based on an Intellidex model, that aimed for more than the generic indexes that dominated the field. Might this be part of that family? As it turns out the answer is “Yes.” Large cap value stocks selected for inclusion rate relatively well in a 15-factor model organized into five broad categories: Price Momentum, Earnings Momentum, Quality, Management Action and Value. The schema and several factors are similar to the Chaikin Power Gauge model that’s part of the Portfolio Wise Power Rank. And like Power Gauge, Intellidex incorporates sentiment-momentum factors I’ve typically used to as proxies for future growth expectations. But there are distinct differences between Power Gauge and Intellidex to suggest that the two combined make for a nice pairing. The PWV portfolio is weighted by a combination of market cap and Intellidex. This is value investing, not just the value factor. Thumbs up.

Advisor Shares Doubleline Value Equity (DBLV) (ETF Home) and SPDR MFS Systematic Value Equity (SYV) (ETF Home): Both of these are “active” ETFs. This is a relatively new area. The traditional ETF, described as “passive,” is rules based. Often, the rules are simple: own every security, or a statistically reasonable sample, in a broad measure of the market, such as the S&P 500. Other indexes are more advanced, such as those built on the basis of rules designed to select stocks that outperform generic benchmarks. (I really hate the word “passive,” which I consider too old-fashioned to cope with the fact that many of these indexes involve lot of brainpower and valuable intellectual property. I prefer to say “rules based” instead of “passive” and “discretionary” instead of “active.” Whatever. SYV and DBLV involve a lot of human judgment as to what makes for a good value investment. On the one hand this suggests the sort of past-performance analysis commonplace among open-end mutual funds. (If the manager was good in the past, we presume they will stay good going forward.) But in Portfolio Wise, we apply our forward-looking Power Rank so we are not actually tied to past performance. I’m intrigued by the potential for genuine value investing with both of these ETFs. But their status as “active,” keeps me at the watching-and-learning stage for now.

Conclusion

I omitted a couple of potentially interesting large-cap value ETFs because AUM and trading volume were much lower than for the ones presented here, and leave me to wonder if either will exist much longer. I also notice, but did not discuss the First Trust Large Cap Value AlphaDex® Fund (FTA) (ETF Home). AlphaDex® is an intriguing methodology but I want to look more closely to better understand why its implementation in large-cap value was, in terms of ETF Group Rank and recent performance, lackluster.

Meanwhile, I’m bullish on QARP, which has the potential to capture an interesting niche in the market. The world has long known about PEG, GARP and the relationship between value and growth. but the relationship between quality and value, QARP, is often overlooked. And good things often happen when one invests in overlooked areas. I haven’t thought much about Intellidex since PowerShares was absorbed by Invesco, but my Portfolio Wise screening exercise told me I need to pay attention again. So I’m watching PWV closely. I’m watching DBLV and SYV — and other active ETFs — but a bit less closely.

Long QARP. May go long PWV.