When I started as an analyst back in 19_none_of_your_business, we rookies typically hid under our desks or in restroom stalls when we knew Lou K, the Assistant Research Director who handled assignments, was looking to unload a pile of utility stocks. Rate base, allowable ROE, regulatory environment, capacity, z-z-z-z-z. Later on, deregulation (sort of) and nuclear plant meltdowns (mainly financial, but a couple for real) jarred the sector from its slumber. Ultimately, though, this remains a relatively ho-hum business. Ditto utility-specific ETFs: There are only eight in our PortfolioWise coverage universe, and most of them generically index the same basket of stocks with little room for variation. All that said, advisers seeking income for nervous clients should definitely stay awake here.

© Can Stock Photo / nicolasmenijes

Ordering A Free Lunch

Every adviser has heard the refrain: “Get me income!” And, of course, there’s the inevitable chorus: “Risk, what risk? No, no.” And just when you think you’ve solved it, bam . . . the mirage.

The Menu

Utility ETFs might just pose a solution.

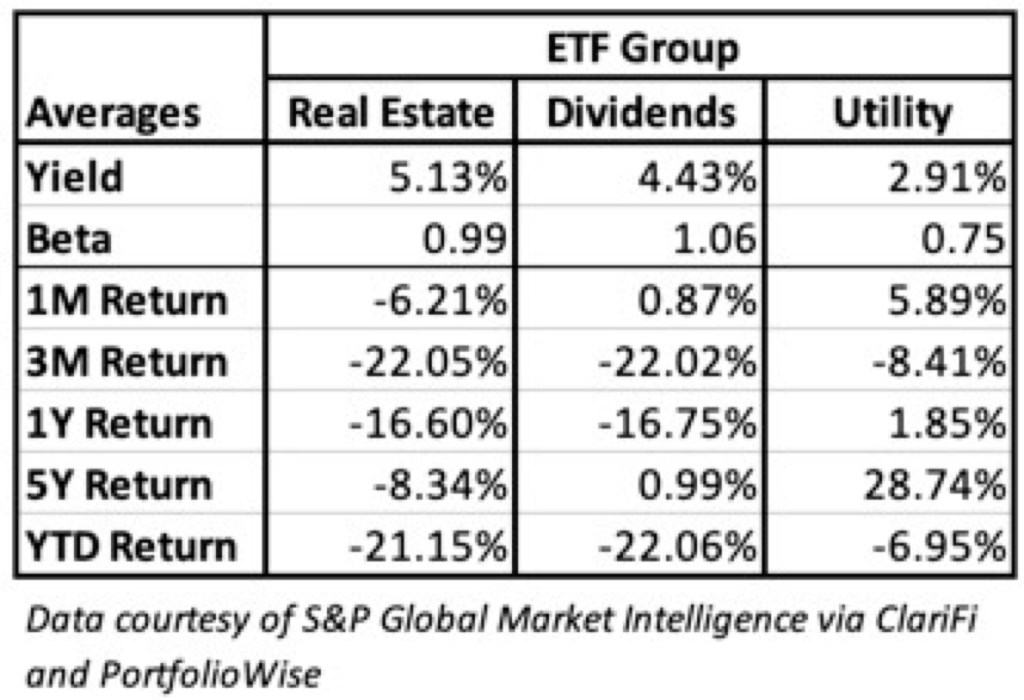

Table 1

Of the three kinds of equity ETFs advisers can tap to generate yield, Real Estate is, on average, tops in terms of yield, the general Dividend ETF category is number two, and Utilities come in third. But when we factor in risk, measured by Beta, the picture changes considerably as Utilities gain power,

© Can Stock Photo / thanapunte5

During the worst of the covid-crash, nothing on the long side of the market “worked” per se. But consistent with what capital asset pricing theory suggested, the pain was far less among low-beta utilities.

Will Utilities Satisfy?

So how much yield should be sacrificed to achieve how much in terms of relative stability of returns? This is an investor-specific question, whether we’re going full-out quant (picking a position on the iconic efficient frontier) or practical (using client-specific risk profiles). But as things stand today, with so much angst about whether we’re in a recovery or a bear market rally, and with considerable uncertainty regarding the extent and pace of eventual recovery from what is, essentially, a planned recession, the lower end of the return-risk spectrum is probably an easier sell now than its been in along time.

XLU: The Main Course

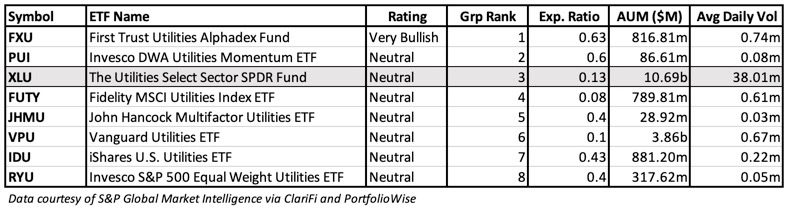

Table 2 shows that the Utilities Select SPDR ETF (XLU) overwhelmingly dominates when it comes to assets under management and trading volume.

Table 2

Are The Side Dishes Meaningful?

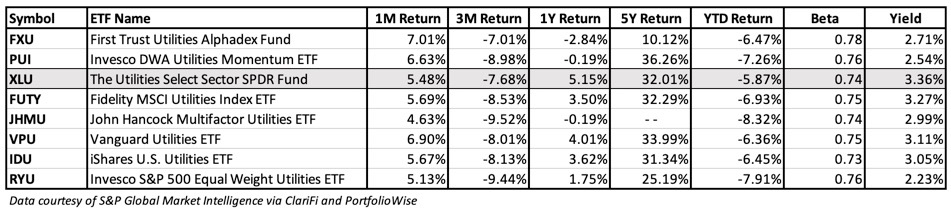

While the data items in the columns of Table 3 are not identical, the extent of variety appears slim. To the extent differences are visible in favor of XLU, they may not be sufficient to pass any sort of statistical significance test. There is, however, one notable exception; a Very Bullish ETF Power Rank for First Trust Utilities Alphadex® ETF (FXU) (fact sheet). The others would have been ranked Bullish but were demoted by a safety-valve technical factor that accounts for the recently-excpetional market weakness.

Table 3

So XLU isn’t a standout; a Michelin-starred entree. It’s comfort food.

© Can Stock Photo / Elenathewise

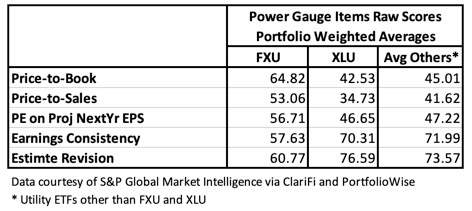

Digging further, Table 4 shows highlights from my examination of portfolio weighted-averages for each of the constituent Chaikin Power Gauge raw rating scores, category scores and individual factor scores. Most differences were except for a few items relating to XLU.

Table 4

Relative to other utility ETFs, FXU’s portfolio is on balance more favorably valued and its earnings rank a but better for consistency, but it has a modestly lesser (but still fine) score for estimate revision. FXU’s yield is also at the low end of the range.

The differences likely reflect First Trust’s Alphadex® selection protocol which tends to favor Russell 1000 stocks highly rated for value or highly rated for growth, as well as a definition of utilities that stretches beyond electric to include gas and telecomm.

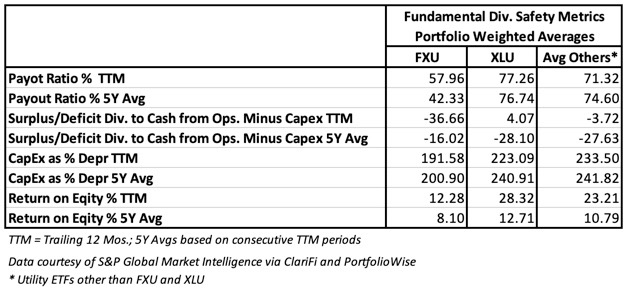

I found a few more differences when I examined portfolio weighted averages for various metrics helpful to analyzing dividend-safety risk, things I hadn’t thought about since hiding from Lou K and his hated stock-assignment memos. Table 5 spotlights those metrics for which any utility ETF — as it turned out, just FXU — stood out from the others in the group.)

Table 5

Here are my observations:

- The lower payout ratios for FXU suggests less risk for stocks in its portfolio, which is consistent with its relatively low yield. By the way, payout ratios in general are adequate (by utility standards), suggesting the companies in which these ETFs invest hav some latitude to tolerate cyclical earnings disappointments without having to immediately take a meat-axe to their dividends.

- The surplus/deficit item is a finer version of the traditional (dividend/net income) payout ratio. That starting point here is not Net Income but Cash from Operations, which is a cash-only version of profit. The traditional income statement includes a subtraction for depreciation, a non-cash accrual that supposedly stands in for capital expenditures; this item is not being subtracted when we look at cash from operations. But given the especially critical nature of utility plant spending, I don’t want to brush “capex” off as discretionary. So I account for it, not with the non-cash depreciation charge but with the actual cash outlay. The surplus/shortfall represents the percent by which dividend payments fit within or exceeded my estimate of adjusted cash from operations. Deficits, unless persistent and exorbitant, are not dangerous; external financing is business as usual in the utility area. The deficits shown by in the FXU portfolio are acceptable, but are worth watching relative to other utility ETFs.

- It’s generally assumed in business that annual depreciation should more or less equal annual capex. The utility group as a whole is characterized by unusually heavy capex. FXU, though, is a tad lighter here; something else that bears watching. Underinvestment could come back to bite in the future.

- Return on equity, always important, is much more so in the utility group. It’s a function of the regulatory environment (how much regulators allow utilities to earn), and how close to allowable ROE a utility is able to get in the real world (this is in turn influenced by regulatory fine print that can make allowable ROE less real than it seems and the utility’s operational effectiveness). Numbers in the FXU portfolio are by no means bad, but they are less utility like, probably reflecting the way Alphadex® pushes the portfolio a bit closer to a conventional equity income portfolio, as well as First Trust’s broad definition of utility.

So it looks as if the data is flagging FXU as a legitimate alternative to XLU; as an ETF that largely shares the same return-risk characteristics but offers a slightly less utilities-intense type of portfolio. The Very Bullish Power Rank and recent share performance (which contributed to a strong Technical component within the Power Rank calculation) suggests that on balance, these differences are for the better.

Those intrigued by FXU might also want to keep eyes on the other non-generic ETFs

One is the John Hancock Multifactor Utilities ETF (JHMU) (fact sheet). It selects utility stocks on the basis of smaller size, stronger share momentum and better company quality. On paper, that looks interesting. But so far in its relatively short (since 2016) history, these differences have not yet been reflected in the numbers I examined.

Also, JHMU’s trading volume and Assets Under Management (AUM) are meager. The securities in the portfolio are liquid so if need be, redemptions (of creation units), if needed, should be manageable. But is a commercial/image risk. If the ETF doesn’t grow at some point, we’d have to wonder if John Hancock might pull the plug. Holders of ETF shares would paid off. But it would be inconvenient and might make for an image problem if an adviser has to explain how it vanished from a client’s account.

If one appreciates the small-size skew in JHMU but is worried about its commercial viability, there is the Invesco S&P 500 Equal Weight Utilities ETF (RYU), where AUM is larger. But in terms of investment merit, the absence of the Quality and Momentum factors included in JHMU give it less appeal and make it suitable only if one absolutely positively needs a utility ETF sans the large-size market cap weighted bias.

Meanwhile, Invesco DWA Utilities Momentum ETF (PUI) (fact sheet) is interesting because of its relative momentum protocol. On the whole, there is enough going for it to propel it to second place in our group ranking. But in terms of the numeric deep-dive described above, we’d have to consider PUI a generalist. Its portfolio seems OK in a lot of things, but not noteworthy in any particular thing.

Conclusion

XLU, by itself, checks all the boxes that need to be checked for lower-risk income exposure and would be a worthy core holding for non-gunslinger clients. As big-name ETFs go, I see no reason to deviate from XLU unless one really has a specific reason to want to favor Fidelity, Vanguard or iShares. Top ranked (per our model) FXU is also appealing. At this point, JHMU and PUI are more suitable for watch-lists with an eye toward future developments.