Expecting to find a “free lunch” in the market (returns potential that exceeds risk) has pejorative connotations, but in reality, anybody who doesn’t strictly adhere to the efficient market theory is, one way or another, trying to accomplish that very thing. In the income area, aggressive practitioners of this approach can expect to hear such phrases as “yield hog” or “sucker yield” and wind up guilty as charged as eye-catching yields turn phantom when dividends get slashed or omitted due to previously-discoverable but often overlooked company financial challenges. Yet with market interest rates still historically low and many investors and advisory clients needing income, the quest for yield can’t easily be abandoned. That adds pressure to turn over more rocks looking for potential traps.

© Can Stock Photo / alphaspirit

The Yield-Total Return Conundrum

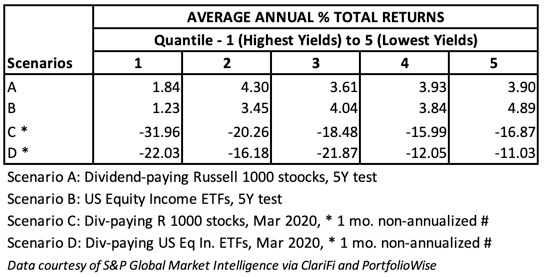

The sucker-yield phenomenon, the inverse relationship between current yield and realized future return, is genuine. Fama-French documented it back in 1988, and I’ve seen it myself many times; Table 1 shows results of some examples. (Notice that even in the March 2020 crash, high yield did not serve as a protective shield against outsized losses.

Table 1

The silver lining in this is that the market itself is fairly adept at recognizing dividend-safety risk, something that is not always as recognizable in standard metrics, such as the payout ratio, as may suppose. This is especially crucial for assessment of income-oriented ETFs where stock-centric data can be challenging to obtain and “roll up” to the level of the ETF.

Assessment of Income-Oriented ETFs

The Chaikin ETF Ratings can be especially useful in evaluating Income-oriented ETFs. The model is based 60% on a three-pronged multi-horizon technical analysis model (which tilts toward the longer view) and 40% on portfolio-level “rollups” of the “quantamental” Chaikin Power Gauge ratings system which covers 20 fundamental, earnings-based, sentiment and technical factors, a suite that is likely to look more favorably on the sort of companies better positioned to preserve and/or grow their payouts. (Click here for a White Paper describing the ETF ratings in detail, or here for a Digest of that paper.)

The ETF ratings are bucketed five ways (Very Bullish, Bullish, Neutral, Bearish, Very Bearish) but given the extent of the market’s 2020 collapse, bullish ratings are hard to come by; almost all US equity ETFs are now rated Neutral or Bearish with the latter category especially well-filled as many otherwise favorably-rated ETFs were demoted out of that category by a market-sensitive safety-valve factor we include (a “technical overlay”). Our ETF-oriented PortfolioWise platform includes a finer level of information: For each ETF “group,” we sort by and present the Group Rank of each member based on our model’s underlying 0-100 score.

Searching For Ideas — Even Now

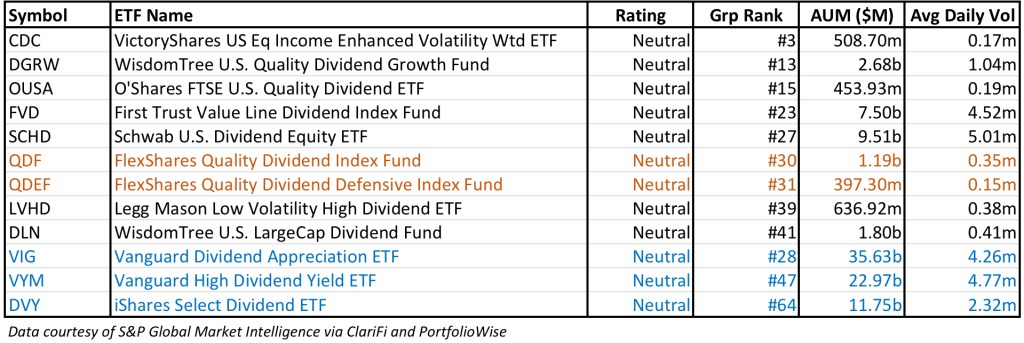

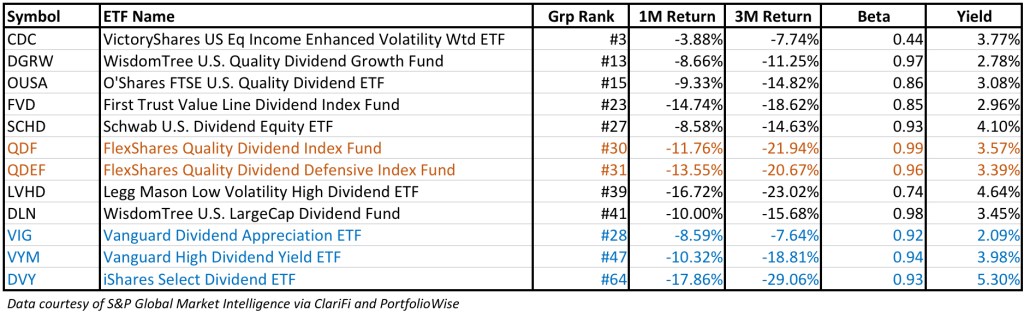

Even those who aren’t adding money to or pulling away from equities should be on the lookout for opportunities to switch from lesser to more promising ETFs within the same strategy. I created an extremely simple screen on PortfolioWise to identify Dividend ETFs with yields of at least 2% that rated no less than neutral. I sorted the result set from best-to-worst based on Group Rank and then visually scanned based on yield and relative performance in the last traumatic month (thus taking cues from the market’s oft-demonstrated proficiency in recognizing the worst candidates) and identified, as worth further review, the ETFs identified in Tables 2a and 2b. (See below for explanations of differently-colored rows.) I particularly confined the list to ETFs that pursue analytic approaches to stock selection and thus eliminated ETFs based on popular dividend aristocrat type themes (except for DVY, which is included because of its popularity and benchmark-like stature), these being a group that warrants a separate post.

Table 2a

Table 2b

The blue rows signify exceptionally large ETFs. There is a strong probability that accounts positioned in Equity Income either own at least one of these, or at least watches them closely for benchmarking purposes.

The brown rows show instances in which I manually adjusted yields produced by the database by subtracting distributions identified by the respective Distribution Schedules published on the ETFs’ web sites as being for other than ordinary income (in these cases, capital gains). This is important: With the market looking to be in a major re-set (new interest rate/fiscal policy/economic regimes), the future may not be so bountiful.

Anomalies Versus Mirages

Our initial impression. of The FlexShares Quality Dividend Index Fund (QDF) and Defensive Index Funds (QDEF), and their “quality” (i.e. lower risk) orientations, suggested free lunches; the yields we initially saw, xx and xx respectively, would be extraordinary if truly accompanied by lower risk. Reality takes over, though, when we restate yield based on elimination of gains distributions and wind up at xx and xx respectively; respectable, but no longer indicative of a free lunches.

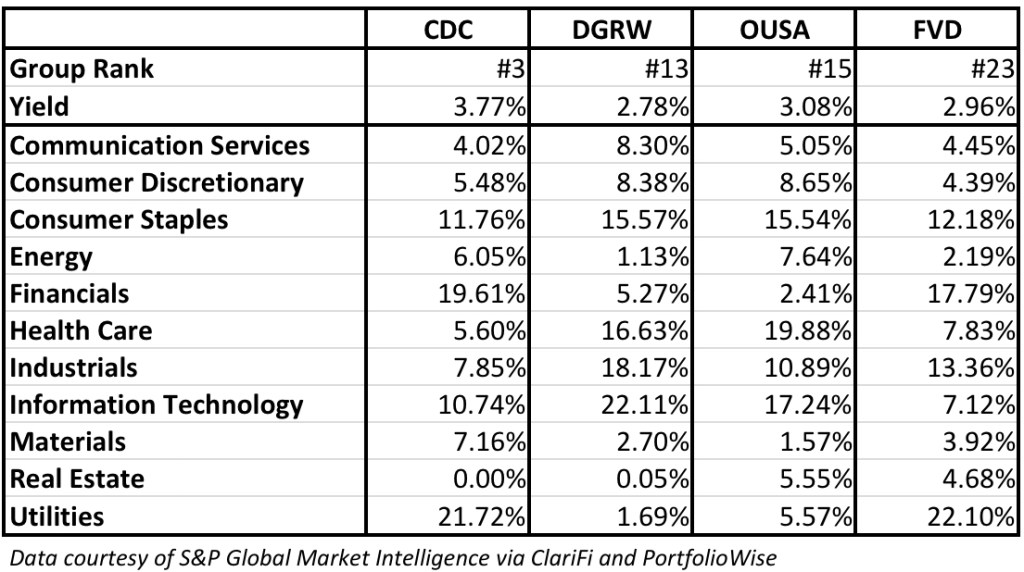

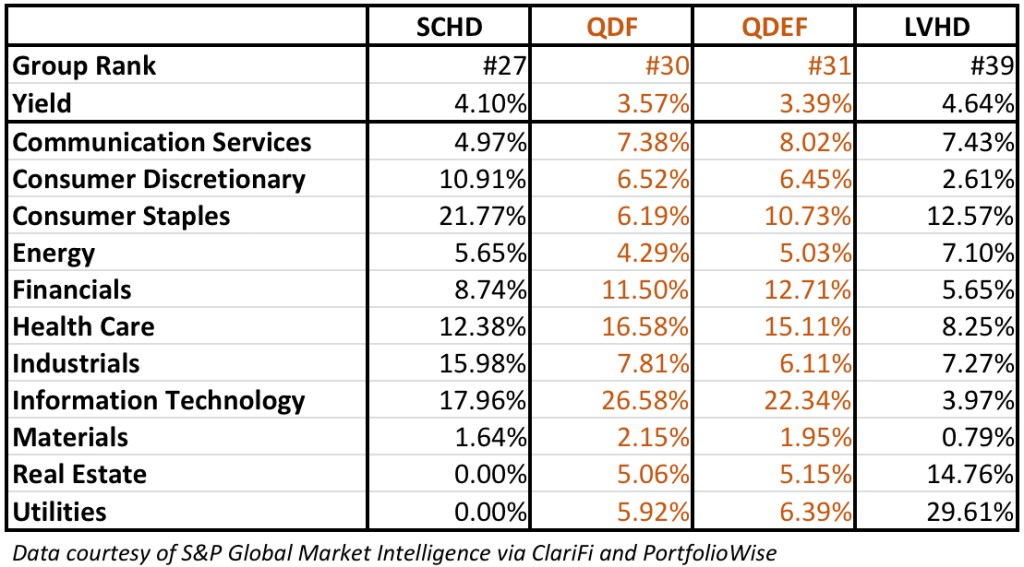

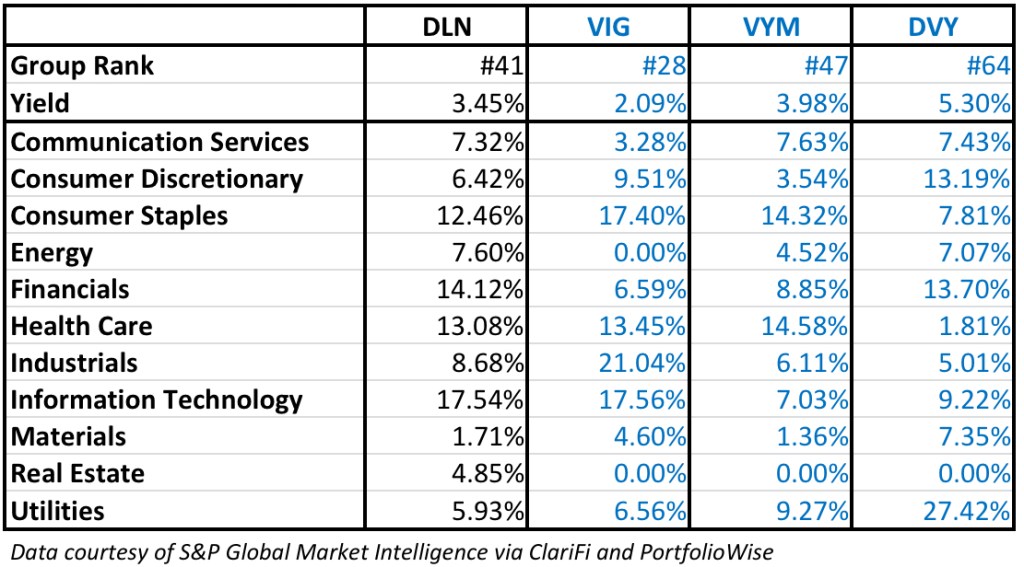

Another source of mirage is inattention to differences in sector exposure. When we examine Table 3a through 3c, we see that allocations go go a long way toward explaining away what first appear to be free lunches.

Higher-yielding funds tend to have more exposure to sectors we consider less appealing. Energy, whose struggles are likely to stretch well beyond the basic economic issues plaguing the market today, are less conspicuous in Tables 3a through 3c than is the case in higher yielding ETFs funds that passed the screen but were omitted from today’s presentation. But even among the groups we ETFs we show, we can see that lower-yielding better ranked ETFs are more geared toward Communications, Healthcare and Information Technology, sectors we view more favorably. Finance and Real Estate have been badly hit lately due to (justified) worries about debt service and rent payments. Consumer Discretionary and Industrials are less intensely cyclical (so far). Least cyclical (but cyclical nonetheless) is the Utilities are, but long-term growth prospects here are relatively modest.

Table 3a

Table 3b

Table 3c

Ultimately, Group Rank and Yield go a long way toward cuing investors into the merits of the portfolio allocations, or at least the Street’s assessment of same.

Choosing ETFs

Start by reading Table 2b from the top down with an initial assumption that this group of ETFs is priced efficiently relative to one another, which, in the context of our approach, means that the differences in Yield/Group Rank accurately reflect a Risk/Quality/Growth-based sort. Checking those that stand out, we note:

The yield for VictoryShares US Equity Income Enhanced Volatility Weighted ETF (CDC) looks in line with sector allocations, but market performance and group rank are being boosted by the ETF’s (1) volatility weighting, giving the largest portfolio allocations to securities that have historically shown themselves to be less volatile (defined as standard deviation of daily performance over the last 180 trading days), and (2) its objective algorithm that shifts percentages of the portfolio to cash when the market is experiencing stress. Risk-averse accounts looking to boost yield should consider rotating some funds into CDC.

Numbers for the iShares Dividend Select ETF (DVY) suggest high risk and lackluster growth potential. Our deep-dive into the holdings, using our Power Gauge stock ratings, supports the Street’s growth assumption. As to risk, however, while there is more than we see in higher ranked ETFs, we don’t see it as fully justifying the ETF’s recent market woes. While we are not fans of the aristocrats-type selection approach DVY uses, given what we see as a misalignment between yield and risk/quality, we would not rotate out of DVY. In fact, we suggest reallocating funds from Dividend ETFs high in yield and Energy exposures — e.g., First Trust Morningstar Dividend Leaders (FDL), iShares Core High Div. (HDV), SPDR S&P500 High Dividend (SPYD), Invesco S&P Ultra Dividend Revenue (RDIV) and Global X Superdividend US (DIV) — into DVY.

The yield on the First Trust Value Line Dividend Index ETF (FVD) seems low relative to its seemingly lackluster sector exposure. But stock selection here is keyed to stocks Value Line rates well for Safety (a rank that combines the company’s Financial Strength and Price Stability ratings). We measure risk differently than does Value Line, but our approach points to similar conclusions regarding portfolio holdings. It does, therefore, appear that this ETF holds is picking better quality stocks within lesser sectors. The safety message being delivered by the modest yield looks legitimate to us.

The two Wisdom Tree ETFs, Wisdom Tree US LargeCap Dividend ETF (DLN) and Wisdom Tree U.S. Quality Dividend Growth ETF (DGRW) may have more appeal than today’s numbers suggest based on the firm’s“dividend weighting” approach, through which it early leader in the “smart beta” field. This has interesting quality-risk control implications given that the economy is likely entering a new “regime” that will automatically re-weight portfolios in line with the flow of dividend payments; Wisdom Tree won’t have to wait a prescribed number of years for the old guard to fade away and newcomers to gain eligibility. For accounts that don’t yet have exposure to Wisdom Tree ETFs, now may be a good time to start dipping toes into the water.