Retail is dead, long live retail! Imperfect, but tolerable. While new approaches to the buying and selling of stuff aren’t quite as much a matter of continuing the old trend as were (as folks assumed or hoped), the succession of monarchs, the reality is that the new era is well investable in terms of quality retail REITs (retail landlords who know what they’re doing) that have to pass the profits through to shareholders.

Why This Idea Is Being Considered

It’s important, before you start to read about or evaluate any idea, to know why the it came under consideration be comfortable soundness of those reasons. Retail REIT Brixmor Property Group (BRX) got into my radar as a result of a High-Quality REIT screen I created on Portfolio123 that searches for the highest yields to be found among (Real Estate Investment Trusts) REITs that have been pre-qualified on the basis of strong “cash on cash returns” (a metric used by real estate investors and operators) and conservative, by REIT standards, use of debt. Details of the approach are described in a 7/5/18 blog post.

Retailing: The Non-Apocalypse

It’s easy to assume brick-and-mortar retail is dead. Who among us in this day and age is still holding out and refusing to buy things on line? I know better to suggest the number is at zero; it takes all kinds to fill a planet. But one doesn’t have to be an investigative journalist to discover that traditional retail isn’t what it used to be; not even close.

It also shouldn’t take an investigative journalist to discover Amazon isn’t now100% of the sector. Even among the most enthusiastic new-tech adopters, it’s clear those wearable fitness gizmos are going to get brutal with users who spend their lives on the couch doing nothing but ordering things on line. We still get out of the house. And there are still lots of things we buy and experiences we have in real life, whether it’s for convenience shopping, fun shopping, or entertainment or even exercise.

What we have, here, is not a retail apocalypse, something that would be unconditionally bad across the board, but disruption, a bold transition to something different, something that will be good for some (those in tune with where the world is going) and horrible for others (those who remain most attuned to what used to be).

Investing in Retail

Passive exposure to retail is probably a very bad idea. We really need to pick and choose here. I took one position in the new era through an unconventional ETF called ProShares Long Online/Short Stores (CLIX) — the name says it all. But I wrote favorably just recently on women’s apparel retailer J Jill (JILL), an up and comer that seems to be growing even though it has, gasp gasp, stores.

We can and should still play retail because we really can’t ignore it; the consumer arena is still about two-thirds of GDP (a bit more at present) and pure on-line isn’t 100 percent of distribution, and besides its mot as if you can expect a bargain with shares of pure online companies.

So as with J Jill, I’m always open to retailers that work in today’s world, and I enjoy hunting for stocks one at a time. But for a one-stop investment that gives me broad-based exposure, rather than a plain-vanilla sector ETF, I prefer to pseudo-feudal-post-modern route; I’d rather be the landlord that makes its money by renting to the outfits that do the dirty work of merchandising, stocking, selling, etc. I could simply develop properties for this, but frankly, that’s way outside my wheelhouse (and I’m not so confident in the region in which I live to put all my eggs in this basket). Years ago big brokerages peddled interests in partnerships, but those were liquidity nightmares.

Today’s Real Estate Investment Trust (REIT) structure gives us a much better vehicle. We benefit from stock market liquidity, geographic diversification, and a business structure that gives us cash returns based on rental profits. We can’t be as hands-on as if we could if we developed the properties ourselves, or had direct communication with and input to the developers and managers. But we do get enough information through public filings that can, if we use them thoughtfully, help us distinguish between better versus lesser outfits. Brixmor shapes up as one of the better firms in this area.

The Business Case

Brixmor leases property for community-oriented open-air shopping venues featuring merchants geared toward everyday convenience, services and in many cases an omni-channel business model.

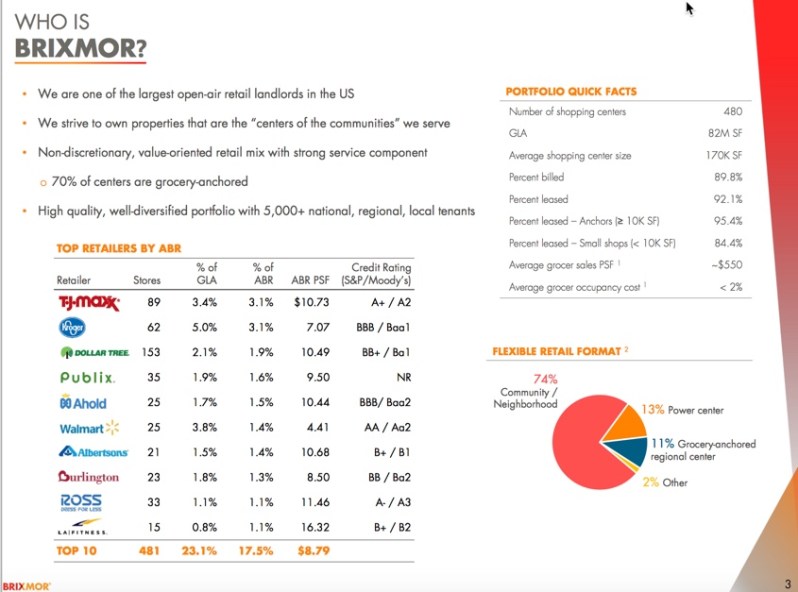

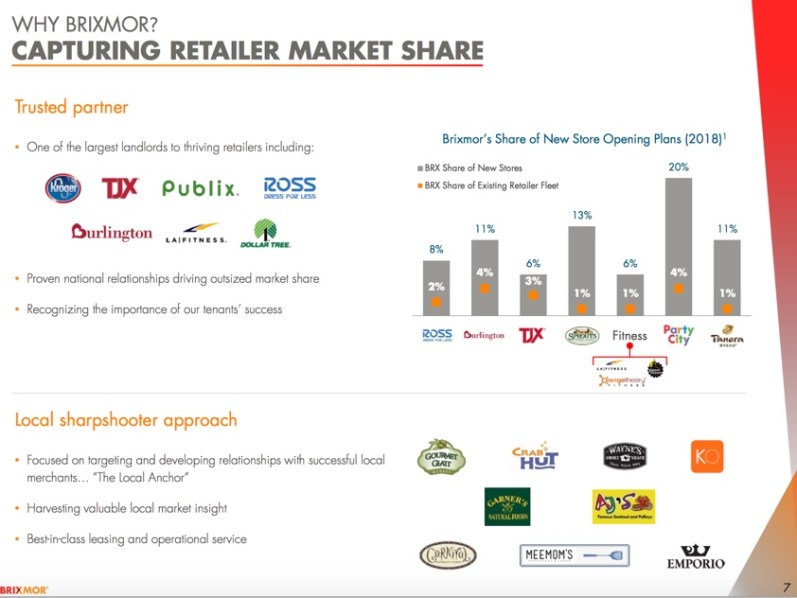

(Images from Brixmor’s 3/31/18 Investor Presentation.)

Omni-channel is a phrase being bandied about a lot in retail nowadays and which is likely to become more prevalent as time passes. It refers to the notion that there is, today, no single way to do retail. Even Amazon signed on to that by acquiring Whole Foods, opening brick-and-mortar Amazon bookstores and installing Amazon lockers that allow customers to receive secure delivery in a wide variety of semi-public spaces. Other merchants have gone to order online and pick up in store; order online and return, if necessary, in store; order in store and receive at home, etc.

Not every retailer will be good at this, just as not every pure brick-and-mortar retailer was good at that approach, or just as not every online merchant is good at that. But the advent of omni channel does empower investors to look at the fundamental numbers and if we like what we see, act on it. We need not dismiss good numbers from any non-Amazon retailer as a phenomenon doomed to falter in the future. Omni-channel merchants feature prominently in Brixmor malls, meaning, therefore, that if the numbers are good, then we can assume they reflect good operations, not a temporary mirage.

There’s also store turnover. Even before the advent of e-commerce, older retail concepts faltered due to changing customer tastes, demographics, management execution, etc. and newer concepts that spoke more effectively to a new generation of customers rose in their stead. The death of long-time dominant local merchant Woolworth did not signal a retail apocalypse nor do the fates of Kmart or or Sears today. Going a few decades into the future, we may even see Amazon and Walmart shunted aside by rivals that don’t yet exist. So be careful about broad brush stories or talking points, etc. Watch the world and look at the numbers to see what’s going on now, and where things are going,

In this sense, playing retail via the REIT rather than the store brands and concepts can be a good thing. It’s fun to pick rising stars here and there, and I’ll do it as eagerly as anyone, But as a portfolio staple, there’s something to be said for riding piggyback on mall operators with footprints on the ground, eyes on customer counts and proficiency in using market rents as the signal that shows where supply and demand are converging and meeting. For a stock market person like me to track the ebbs and flows of retail (without chasing stocks that already soared in response to surprises of plummeted in the wake of disappointments), it’s more like a hobby. For mall operators, its day-to-day business.

A REIT like Brixmor won’t likely give you the chance to double, triple or quadruple your money or better as you could by latching early onto an emerging concept or operator. But this sort of vehicle can help you control risk and generate a reasonable dividend stream, something that may not have been cherished much during the decades characterized by the plunging-interest-rate-driven stock boom, but which could become better appreciated if, in the future, stock market investors have to work harder for gains by searching for better businesses with better earnings growth rather than throwing darts and counting on Uncle Fed to make all thing right.

The Numbers

Lets start with dessert, the yield.

Table 1

| BRX | Medians | ||

| Peers | All REITs | ||

| Div Yield % | 6.31 | 4.71 | 4.12 |

| Div Growth % 1Y | 6.12 | 4.92 | 7.14 |

| Div Growth % 3Y | 12.68 | 5.15 | 5.57 |

| Div Growth % 5Y | NA | 7.20 | 8.17 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols, TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Retail REITs.

It’s obvious that this is fine. So let;’s move on to Table 2, which depicts dividend coverage.

Table 2

| BRX | Dividends as % of Funds Fr Oper | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 50.99 | 71.05 | 72.06 |

| 2017 | 49.72 | 70.08 | 72.54 |

| 2016 | 46.71 | 63.26 | 67.98 |

| 2015 | 44.70 | 67.65 | 65.81 |

| 2014 | 31.21 | 68.50 | 67.59 |

| 2013 | 13.00 | 64.33 | 65.71 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Retail REITs.

We’re still rolling.

Tables 3 and 4 show the key fundamentals, cash on cash return and leverage.

Table 3

| BRX | Cash on Cash Return (%) | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 22.07 | 13.80 | 11.78 |

| 2017 | 22.00 | 14.31 | 11.67 |

| 2016 | 21.67 | 15.62 | 11.72 |

| 2015 | 20.55 | 14.64 | 10.77 |

| 2014 | 19.06 | 11.98 | 9.60 |

| 2013 | 12.59 | 12.42 | 8.65 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Retail REITs.

Table 4

| BRX | Leverage (Total Debt 2 Eq) Ratio | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 1.96 | 1.57 | 1.15 |

| 2017 | 2.02 | 1.46 | 1.17 |

| 2016 | 2.00 | 1.47 | 1.09 |

| 2015 | 2.08 | 1.59 | 1.21 |

| 2014 | 2.07 | 1.50 | 1.18 |

| 2013 | 2.54 | 1.45 | 1.13 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Retail REITs.

The cash on cash returns are impressive. They’re well above retail-REIT and all-REIT medians, This is the functional equivalent of a very high Return-on-Equity corporation. I love that. It shows Brixmor its doing a really good job running its malls, acquiring at good process, operating efficiently, getting good tenants, etc.

We do, however, raise an eyebrow at Brixmor’s willingness to utilize debt. The leverage ratio is not bad, but it is above comparative medians and is at the upper boundary of what I’m willing to accept. The magnitude and consistency of Brixmor’s cash on cash returns helps me tolerate it

And it’s not as if a REIT leverage ratio in the vicinity of 2.0 make Brixmor a gunslinger. Simon Property Group (SPG), by far the largest and possibly best known retail REIT, has a leverage ratio in the vicinity of 6.0. Simon’s cash on cash returns have been over 100% so it’s not as if the big gorilla lacks skills. It just so happens that I prefer to refrain from going that far out on the reward-risk limb, especially when Birxmor gives me a higher yield, 6.3% versus 4.6% for Simon.

Conclusion

Brixmor works for me in several ways. I understand retail, even the contemporary approaches to it. I think Brixmor’s exposure is probably more stable than many in the sector. I like the yield, and I like the business fundamentals from which the distributions spring.

2 thoughts