Given the rising proportion of the US population that has and continues to attain senior-citizen status, and the high demand for health care services of all kinds among seniors, you’d think this would be a no-brainer investment opportunity. Money and the politics around it have frustrated such ideals, so no investment in this area is a slam-dunk. But National Health Investors (NHI), a good-yielding REIT, comes as close to it as anything I’ve seen.

Why this Stock is Being Considered

It’s important, before you start to read about or evaluate an idea, to know why the it came under consideration be comfortable soundness of those reasons. National Health Investors (NHI), got into my radar as a result of a High-Quality REIT screen I created on Portfolio123 that searches for the highest yields to be found among REITs that have been pre-qualified on the basis of strong “cash on cash returns” (a metric used by real estate investors and operators) and conservative, by REIT standards, use of debt. Details of the approach are described in a 7/5/18 blog post.

Whetting The Appetite

We all know how hard it is to find a decent yield nowadays. The S&P 500 SPDR ETF (SPY) yields about 2.4% and as for fixed income, we can only dream of getting to that level unless we take on a lot of market risk (the possibility that rates may rise from today’s epoch low levels and cause principal values to fall) and/or credit risk. So National Health’s yield situation definitely raises an eyebrow.

Table 1

| Medians | |||

| NHI | Peers | All REITs | |

| Div Yield % | 5.26 | 5.52 | 4.12 |

| Div Growth % 1Y | 11.71 | 1.64 | 7.14 |

| Div Growth % 3Y | 7.19 | 4.38 | 5.57 |

| Div Growth % 5Y | 7.44 | 6.50 | 8.17 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols, TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Healthcare REITs.

We see that REITs in general and Healthcare REITs in particular also have good yields, but National Health stands out in the way it combines yield with a historic track record of good dividend growth, Yes, the past is the past and we care about the future so we won’t use the growth record to aspire to any sort of dividend aristocrat stature (which we couldn’t do anyway since the very nature of a REIT is inconsistent with perfect quarter-after-quarter or year-after-year dividend trends). But it does at least make for a nice jumping off point to get us into the business itself.

The Business

National Health, as a Real Estate Investment Trust, is a landlord. Its portfolio of properties are all leased to operators of health care facilities that serve elderly clients. Traditionally, we think of this as being nursing homes, and that is part of National’s business mix. But the field has evolved over the years to accommodate a wide variety of seniors with differing physical and mental capabilities and differing needs for care. Nursing homes are for those with substantial needs. For others, there is senior living, assisted living, memory-care facilities, skilled nursing, etc.

The advent and growth of such lower-intensity care facilities as assisted living and senior living mean people engage with such facilities often while health is still generally sound and remain so engaged for long periods of time. For many in National’s orbit, its not as if they are stuck away in facilities; many choose to be there for companionship with other residents, activities oriented toward seniors, and freedom from such tasks as maintaining their own living spaces, laundry, shipping, cooking, getting to medical appointments, dressing and grooming for many, etc. not to mention the benefit of having some sort of care nearby 24/7 in case of unexpected need.

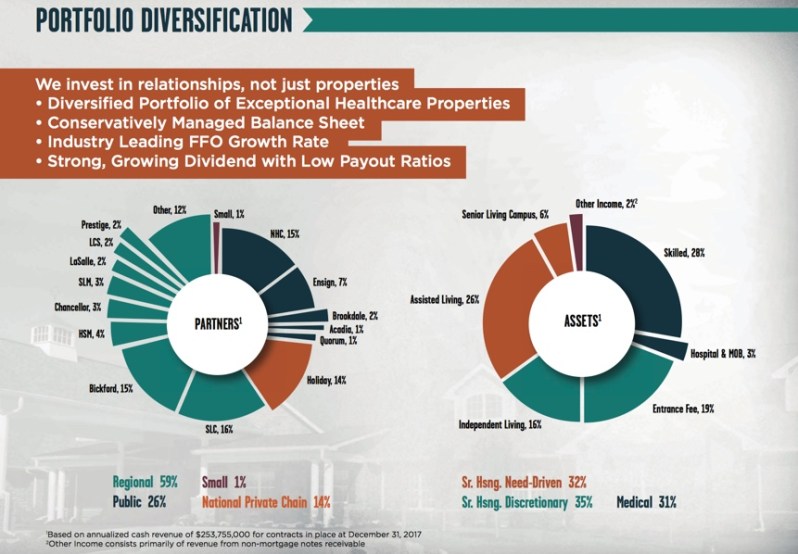

Figure 1

Figure 2

(Figures 1 and 2 from NHI 2018 Annual Shareholders Meeting Presentation.)

Many readers have already come into contact with this sort of thing, if not for themselves then for parents, uncles, aunts, etc., and those who haven’t so far can expect to do so at some point. Father Time says so and Father Time always gets his way.

So demand for the facilities leased by National is strong and is absolutely positively going to grow unless a generation of baby boomers vanishes prematurely such as through the scheme put forth in Christopher Buckley’s hilarious satirical novel Boomsday. National does face risk the same way every landlord does, mainly related by the ability or willingness of tenants to pay rent. But with a field as “inevitable” as the one in which National’s tenants operate, you’d think risk is for other REITs, not National. Unfortunately, though, if you think this way, you’d be wrong. Some way, some how our society has managed to make a boondoggle over even this. I won’t go into all the handwringing over how everybody wants everything but wants to pay for nothing and the myriad of dysfunctional ways supply sand demand manage to intersect. Suffice it to say that providers of aging-related health services struggle to get paid. Being a landlord keeps National off the front lines as even challenged businesses know they’d better at least pay rent. But at some point, National’s rental income will have to have a reasonable relationship with what its tenants can afford to pay.

So, we’ve had some good news (a business that needs to exist and will grow) and bad news (it’s not immune to risk related to monetization). Now, let’s get back to good news.

Looking Ahead

First, I’ll engage in some political speculation. There’s an old-time cliche that a conservative is a liberal who has been mugged, or a student activist who gets a family and a mortgage. Along the same lines, I’ll suggest that one who opposes generous becomes a big-time advocate when a parent needs 365/24/7 attention (even Ayn Rand wound up taking Medicare and Social Security), and as Father Times continues his march through Baby Boomer Country, more and more such conversions of faith are likely to occur. I can’t predict exactly how all this will eventually shake out, but I believe it somehow will. Investing in equities, a risk asset, always requires some sort of a leap of faith, and as such leaps go, this one isn’t half bad, especially if you can collect a decent dividend while wincing at whatever babble is “trending” at the moment.

A Strong Operator

Second, National has already exhibited a level of operating proficiency that can justify an assumption that it has the potential to whether challenges and prosper from favorable developments.

As explained in my 7/5/18 post, cash on cash (COC) return is an important measure in real estate. Good numbers means the operator is getting properties at good prices, doing a good job in monetizing what it has and/or keeping expenses in line. Table 2 shows where National stands relative to REITs in general and Healthcare REIT peers.

Table 2

| NHI | Leverage (Total Debt 2 Eq) Ratio | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 0.88 | 0.99 | 1.15 |

| 2017 | 0.87 | 0.97 | 1.17 |

| 2016 | 0.92 | 0.96 | 1.09 |

| 2015 | 0.81 | 1.11 | 1.21 |

| 2014 | 0.83 | 1.14 | 1.18 |

| 2013 | 0.81 | 1.07 | 1.13 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Healthcare REITs.

Table 3 shows that National’s balance sheet is a near (a tiny bit better) than the REIT and Healthcare RET norms, which is a very good thing: Above average returns accompanied by only average financial risk: Sign me up!

Table 3

| NHI | Cash on Cash Return (%) | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 16.81 | 10.83 | 11.78 |

| 2017 | 17.24 | 10.33 | 11.67 |

| 2016 | 15.74 | 10.88 | 11.72 |

| 2015 | 15.63 | 8.29 | 10.77 |

| 2014 | 11.12 | 8.99 | 9.60 |

| 2013 | 8.34 | 8.34 | 8.65 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Healthcare REITs.

What does all this mean for the next quarter or for whether National will beat, meet or miss guidance? Darned if I know — or care. Those who are familiar with my work know I don’t play that game (although I’m not averse to trying to profit off others who do; see, e.g. a prior post on an EPS Surprise screen I created). Aside from the big picture, my concern here is the sustainability (at least, and preferably prospects for growth) of the dividend. REITs aren’s as smooth as regular corporations that can and do keep lots of rainy-day surplus that allows them to pay more than they take in during off years. But as REITs go, I think National is on solid ground given that its payout is amply covered by Funds From Operation.

Table 4

| NHI | Dividends as % of Funds Fr Oper | ||

| Medians | |||

| Peers | All REITs | ||

| TTM | 70.58 | 87.01 | 72.06 |

| 2017 | 67.57 | 85.79 | 72.54 |

| 2016 | 67.27 | 78.31 | 67.98 |

| 2015 | 62.41 | 87.37 | 65.81 |

| 2014 | 72.57 | 87.56 | 67.59 |

| 2013 | 83.81 | 89.75 | 65.71 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols as well as ratios created by the author. TTM = Trailing 12 Months, MRQ = Most Recent Quarter. The Peer group refers to Healthcare REITs.

The potential for dividend growth is especially crucial nowadays, since interest rates, still near generational lows, are much more likely to trend up than otherwise. REITs ad other income stocks got slammed viciously not long ago based on such fears. It might happen again — at least for a while, But eventually, I expect the multitude of investment-community participants who are not old enough to have experienced anything other than falling rates will eventually come to realize that rates, if they rise, will likely do so based on prolonged economic strength and if that happens, companies (and REITs) should be better positioned to raise dividends, something that can’t happen in fixed income because there the income stream is, well, “fixed.” (I suppose we could rename equity income to unfixed income.)

Conclusion: Partnering with Dr. D

I’ve long been attuned to the Baby-Boomer demographic surge and all it implies. I’ve also long been frustrated by how hard it has often been to monetize and invest in this area. Insurers don’t want to pay for new drugs, equipment etc. Hospitals would prefer to not spend on care and I’m sure, if they could ever get their lawyers to say “yes,” introduce outpatient organ transplant surgery. I’ve given up reading about the trials and tribulations of the Affordable Care Act and all it touches. As I said above, nothing in healthcare, not even National, is completely immune to all this. But all things considered, National may be the single most investable idea I’ve come across that’s tied to Dr. D (Demographics).