If there’s one thing that’s plentiful on the internet today its commentary on Real Estate Investment Trusts and plenty of interested investors eager to consume it. Much of it, however, consists of largely subjective fundamental judgment. That’s fine. There are some good people doing it and I subscribe to some their services. What seems to be missing, though, is a primarily quantitative market-oriented point of view. My aim here is to start to fill that gap.

© Can Stock Photo / EyeMark

Applying The Chaikin Approach To Real Estate Investment Trusts

The Chaikin Power Gauge model is a 20-factor fundamental/technical protocol based not on statistical data mining but on the experience of Wall Street veteran Marc Chaikin in terms of how successful investors invest, which distinguishes it from the Fama-French inspired generation of academic-type formulations.

As with most models that address fundamentals, conventional financial statement items and valuation metrics are utilized. REIT investors, however, tend to work with different sets of numbers. These correlate loosely with traditional Power Gauge factors; enough so to allow one to get by using the full model. But I find that the effectiveness of the approach can be significantly enhanced by (i) eliminating from the outset the highest yields, the ones that suggest bearishness on the part of Mr. Market, and (ii) paying extra attention two of the four Power Gauge factor categories, Earnings Growth and Expert Opinion and allowing for consideration of REITs with Neutral or better overall ranks if the sub-ranks for these two categories are also neutral or better.

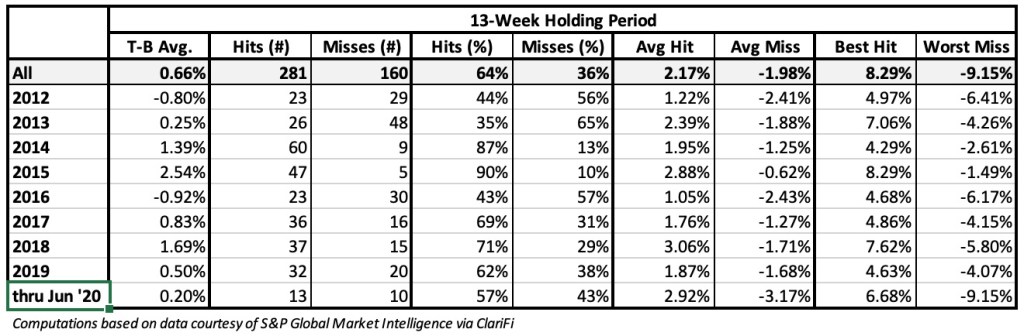

Table 1 shows the results of a backtest of this flexible approach; it covers the period of time during which Power Gauge was in live use. The analysis is based on T-B (Return of the Top Group minus return of the bottom Group) and Hits versus Misses (T-B being positive is a “Hit.”) Since this is a screen based analysis rather than a typically ten-“bucket” academic study, I use only two groupings; the Top consists of the group of REITs that satisfied my criteria,; the Bottom refers to all other REITs, those that failed.

Table 1

Picking Specific REITs

However much modeling one wants to do, it’s important today to be concerned with rent collection, the extent to which tenants are“essential.” Power Gauge’s sentiment-based factors indirectly pick up on this by tapping into collective investment-community judgments, and now, with a post-covid quarter in the books, even some of the more conventional numbers can contribute here. In any case, quant should never be a do-or-die dogmatic thing. It should be used to assist human judgment, not eliminate it.

Housing REITS

Nothing is more essential than housing. That doesn’t mean smooth sailing for REITs that operate in this area. People who are out of work or struggling under reduced work hours due to their workplaces having been limited by covid often cannot afford to pay rent, and various branches of government have imposed moratoriums halting evictions. Tenants remain liable for rent arrears they accumulate. The unfortunate reality today is that landlords are having to live with rent defaults and for real estate investment trusts, that quickly translates to reduced or eliminated dividends.

But not al REITs are alike. Their portfolios include properties in different parts of the country some of which are considerably better, economically speaking, than others. Housing REITS vary, too, in the scale (upscale/downscale) of their properties.

The screen is showing us two housing REITs both of which have Bullish Power Gauge ratings; BRT Apartments (BRT) and Front Yard Residential (RESI).

BRT, which focuses on mid-level multi-family units in growing sunbelt markets, has been collecting about 98% of its billed rents so far. Its dividend payout ratio, about 95% of FFO (Funds From Operations — the key cash-flow like REIT metric) is very tight, we should not be surprised to see a dividend cut in the near future. But with the yield near 7%, it appears Mr. Market is already expecting that. Looking beyond covid, though, BRT has good growth opportunities due to its favorable geographic exposure, access to new projects (helped mainly by joint venture partners with local expertise) and rent increases due to upgrades of so-so apartments.

RESI, yielding 4.75%, is another sunbelt-focused landlord but this REIT emphasizes the renting of single family houses. RESI’s rent-collection experience has been excellent to date; nearly 100% in July and in the preceding months was in the high 90s. Debt leverage is high even by REIT standards, but the FFO payout ratio, at about 65%, is more palatable. Back in February, RESI had agreed to be acquired but when covid hit with all its uncertainties, that deal was terminated, although RESI did receive a $100 million termination fee. The stock reacted as one would expect — horribly — but it’s been climbing back in light of improving rent collections and the clear signal from management that it is willing to be strategically bold.

Industrial REITs

These could go either way when it comes to “essential” and rent collection.

Duke Realty (DRE) and Granite Real Estate (GRP.U) (U.S. trading shares of a Canadian REIT) are both neutrally ranked and pretty solid; both have yields, 2.45% and 3.72% respectively, that are below fear levels. Their respective FFO payout ratios are 64% and 63%. Debt levels are low relative to he REIT world. The key to both reflects the essential, increasingly essential some might say, nature of the tenants’ activities — distribution and logistics.

Plymouth Industrial (PLYM), yields 6.16%. That tells you Mr. Market feels a greater sense of concern. The REIT focuses on Class B properties about evenly divided between warehousing and light industrial. Rent collection has been running in the low 90s percent-wise. The FFO payout ratio here is a modest 40% — but this is after the REIT just cut its quarterly payout from $0.375 to $0.20 (the yield is based on an assumed four quarters worth of the $0.20) payout. My interest here reflects the fact that the dividend has already been cut to affordable levels, the stock has already discounted potential dilution from a planned secondary share issuance, and when the economy normalizes, the Class B emphasis should look good (glamor is nice; low investment can be nicer).

A Storage REIT

This category of real estate investment trust has fans and naysayers. Demand for storage ebbs and flows but on the whole is healthy. But the supply of storage has grown. That’s a potential problem and a reason why the yield for National Storage Affiliates (NSA) is 4.02% and not lower. Another factor: the FFO payout ratio, at 84%, is higher than many would like to see. Actually, though NSA raised the dividend by a penny a share in the most recent quarter, so there have to be other things to consider. The main thing is probably the way NSA operates. As detractors suggest, anybody with a piece of land can open a self storage business (it’s easy to operate). But as anybody who has ever looked to rent storage knows, its not so easy for fly-by-night operator John Doe to get the best located properties or have the knowhow or wherewithal to attract customers. The big guys, the one with resources and scale, are the ones with bona fide market presence. NSA is one of the big guys, and its growth efforts are helped with its use of joint ventures and subsidiary-line autonomous PROs (Participating Regional Operators). Rent collections, meanwhile, are normal.

The Belly Of The Beast: Office and Retail REITS

Ouch! With the way people are working from home and shopping online now and with many likely to continue doing so, if not permanently, then long after the health crisis passes, you’d think any real estate investment trusts in this area would be toxic — and many are. But not all.

Office REIT Cousins Properties (CUZ), with a yield of 3.87%, is ranked Bullish under Power Gauge and is triggering a Chaikin Reversal Buy signal. Not surprisingly, occupancy is down significantly as people work from home, but percentage rent collections have been in the high 90s. The REIT focuses on southern cities experiencing net in-migration, including for office workers. Debt is modest — in fact, CUZ’s Bullish Financial category Power Gauge rank is almost unheard of in the REIT world. The FFO-payout ratio is a modest 43%.

Whitestone REIT (WSR) is the white-knuckle choice. It’s a retail REIT — but not malls. It has neighborhood centers in high income areas in business-friendly growing areas; Phoenix and Texas (Houston, Dallas Austin and San Antonio). Using “psychographics” (analogous to what “analytics” does in sports), WSR carefully orients its properties to chosen consumer types. Even so, covid is covid and rent collection had been bad(63% early in the pandemic) but it’s getting better (81% in the second quarter and 86% in July). Debt is reasonable and the dividend has already been reduced. The FFO payout is now a comfortable 44%. The current yield, 6.22%, reflects the riskier tenant base, but all things considered, seems high given the specific situation here. The Power Gauge rating is Bullish.

Holding disclosure … Long BRT, CUZ, DRE, GRP.U, NSA, PLYM, RESI, WSR

#RealEstateInvestmentTrusts #REITs, #RealEstate, #Yield #Dividend, #Income $BRT, $CUZ, $DRE, $GRP.U, $NSA, $PLYM, $RESI, $WSR