Fed Chair Jerome Powell may be a Godsend to the Covid-era financial markets, but to retirees, he’s the Scrooge-like boss that keeps pushing wages down toward what has to seem like starvation levels. That’s what the aggressive interest-rate reductions have to feel like to those who aren’t borrowing to launch new businesses but are instead, relying on investment income to live. Lest we be too tough on the guy, we do have to at least remember that the Fed’s liquidity onslaught has done much to rescue principal values from the abyss into which they seemed to be headed back in March. Even so, those who need current income have to do something.

© Can Stock Photo / gajdamak

Finding The Sweet Spot

It would be wonderful if retirees could simply sort investment candidates by yield and pick from the top. But the R-word (“Risk”) rains on that parade. Mr. Market is no fool. If the yield is very high, it got that way not because the income is great but because the principal value plunged in response to (often well-founded) fears that the company or issuer won’t be able to keep paying out the money. On the other hand, as we reduce risk, we find our potential returns likewise diminishing.

Unless particular circumstances force an investor to cling to the lowest extremes on the risk scale (where returns remain painfully close to zero), compromise becomes the order of the day. We’ll need to take at least a little bit of risk and tolerate an income level below what we’d ideally want. The good news is that the middle ground can be a real sweet spot in the income-investing world.

Let’s think of this sweet spot not as a pinpoint bull’s eye but as a range. Those who can and want to move a little to the high side of the center of the reward-risk scale can consider ETFs that invest in good-yielding stocks. Click here for more on Dividend ETFs in general and here for more on Utilities (the traditional source of dividend income). Today, we’ll consider fixed income, the more conservative side of the sweet-spot range.

Searching For Fixed Income ETFs

Fixed-income yields today typically won’t match what can be found among the kinds of stocks dividend-seekers tend to favor. For retirees, the choice to accept a lower yield is about risk; less price volatility for fixed income and less risk of income suspension or discontinuance.

But beyond the risk/reward profile, fixed income securities and fixed-income ETFs differ structurally from their equity cousins and require a different set of decisions.

- With the fixed-income market hovering near a mathematically-defined ceiling (caused by near zero interest rate and the reality that so-called negative interest rates don’t really mean retirees can look forward to the sort of bull market we’ve seen in security prices that has felt almost automatic for much of the past 40 years), we should be happy if ETF prices can hold their current levels or not fall too much. In contrast to stocks, capital gains are not nearly as important in fixed income. In fact, if interest payments are large enough, capital losses are perfectly respectable. ETF owners who are able to reinvest income can also look forward to increases in number of shares owned.

- Recognizing that interest rates can no longer fall to an extent appreciated by anyone other than traders, I’m eliminating ETFs that emphasize longer-term securities, where risk of loss from potentially rising rates is greatest. Right now, the yield curve (the higher interest rates investors receive for taking the risk of owning longer-term instruments) is not enough, in my view, to induce retirees to chase them. So I’m aiming at ETFs that emphasize short and intermediate time horizons.

- I’m looking now at ETFs that emphasize investment-grade corporate issues. I’m not sufficiently confident in the economy to pursue high-yield junk bonds (the stock market seems to be expecting a vigorous recovery, but retirees may not want to take the risk that the scenario envisioned by equity investors may turn out wrong —especially if we have a second coronavirus wave). At the other extreme, lowest-risk Treasury yields are too low.

- I want ETFs that are rated Bullish or Very Bullish according to our Power Ranks. The number of such offerings that satisfy my other constraints is ample, so I see no reason to select ETFs ranked Neutral or Lower.

- Assuming as I do that retirees are a risk-averse group, I limit consideration to ETFs that are rated no higher than Moderate for Volatility and below 1.00 for Beta traditionally, Beta is computed relative to something like the S&P 500, but for fixed income, our Betas compare volatility of individual ETFs to the broadly-represented iShares Core U.S. Aggregate Bond ETF (AGG) (ETF Home).

Three Income Ideas For Retirees

Given my focus on investment-grade corporates, it seems obligatory to start by mentioning the iShares Iboxx $ Investment Grade Corporate Bond ETF (LQD) (ETF Home), the huge (assets under management: $52.45 billion) bellwether in this area which, by the way, carries a Very Bullish Power Rank. But I’m not going there. With the fixed-income market being where it is, scraping against its mathematical ceiling, I’m going to pass on its high 1.36 Beta, something that likely came about because of above-average exposure to longer-term securities that are more vulnerable to declines if/when interest rates rise in the future. (They would generate greater gains if interest rates continue to plunge, but given where rates are now, common sense suggests that the risk-reward choice has shifted no lots of potential risk with no meaningful likelihood of meaningful upside capability).

I’m instead going instead offer three fixed-income ETFs that have the potential to deliver decent income (as decent as one can expect nowadays) without taking imprudent risks. These are not the usual household names, but that’s probably a good thing. What Peter Lynch wrote long ago about stocks to lead off Chapter 9 of his classic One Up on Wall Street (“If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favorable publicity, the one that every investor hears about in the car pool or on the commuter train—and succumbing to the social pressure, often buys.”) can apply to ETFs as well (so long as small AUM doesn’t exacerbate commercial risk) applies here too.

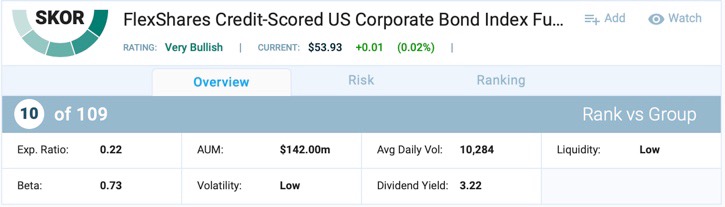

FlexShares Credit-Scored US Corporate Bond Index ETF (SKOR) (ETF Home):

Images from PortfolioWise – Powered by S&P Global Market Intelligence/ClariFi

SKOR is small, with an AUM of just $142 million. While I don’t think that is so small as to cause commercial risk: FlexShares (a division of Northern Trust) has some larger ETFs but for the most part, it’s a niche firm that aims at research-driven specialty ETFs, as opposed to blunt-force asset-gathering associated with the giant generic funds. SKOR’s place within the overall lineup does not suggest any temptation on the part of Northern to disband it any time soon. Quite to the contrary, its fixed-income offerings as a whole are very well rated by us and I can readily envision this issuer gaining stature in the new, much more challenging, fixed-income era now starting to unfold.

This is a passive ETF in that it follows a disciplined strategy. But I think the term passive is really a misnomer for this sort of fund: I prefer to call it a model-based approach since there is a lot of picking and choosing (by an algorithm as opposed to a human) in an effort to do better than a truly passive own-everything index.

With SKOR, it’s all about fundamental analysis analogous to what humans and more thoughtful equity ETFs do with stocks. The yield, even with the mental reduction one should apply in order to address portfolio rollover risk in today’s environment, is likely to be quite respectable in light of the overall short-intermediate term risk, which is reflected in the Low volatility and a beta that is below 1.00.

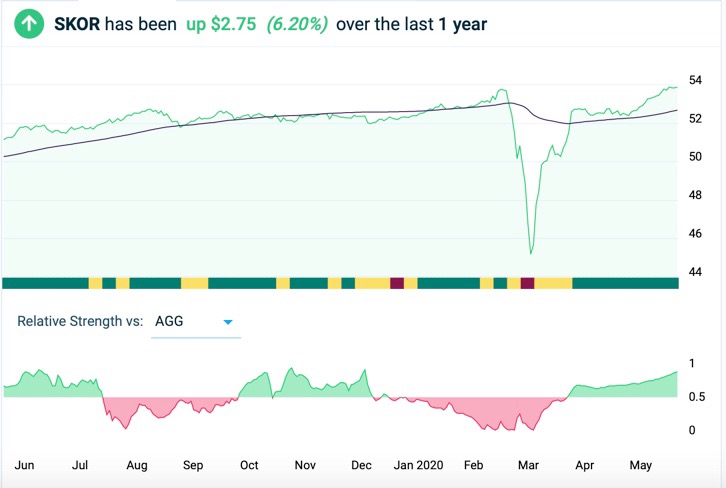

Franklin Liberty Investment Grade Corporate ETF (FLCO) (ETF Home):

Images from PortfolioWise – Powered by S&P Global Market Intelligence/ClariFi

The most noteworthy aspect of FLCO is that it’s an actively-managed ETF. In other words, it is not rigidly confined to a broad-basket of securities, nor is it even confined to a list created by an objective model. This is obviously a controversial quality, especially in stocks, where academics, gurus and commentators have complained for decades about active portfolio managers being unable to beat the market consistently. It’s also controversial in the ETF world, with its need for continual holdings disclosure.

I don’t want to wade into the broad active-versus-passive debate right now except to say that in fixed income, I like the idea — at least under present market conditions. All passive or model-based protocols are necessarily based on data from the past with the challenge being to find ways to use that information in ways that can support credible assumptions about the future, which is what what we do with our equity Power Gauge ranks and our ETF Power Ranks. But when a market has been trending one way for nearly 40 years and then smacks up against an impassable wall, as is the case in fixed income, there is something to be said for the human element. It’s not that modeling is necessarily absent. But when brought to bear, as with this ETF, it’s part of the process, not the whole thing.

This is why I’m willing to accept, for FLCO, a moderate level of volatility, reflecting a longer term structure than I’d assume for ETFs with Low or Very Low volatility. I understand that the managers have the ability to shorten up when the need to do that is perceived, something a passive or purely model-based manager cannot do.I also appreciate the ability of a manager doing fundamental credit analysis to comfortably reach for more yield than one who is not able to exercise judgment.

The Bullish Power Rank and healthy Group Rank together tell us that the managers here have been doing a good job so far.

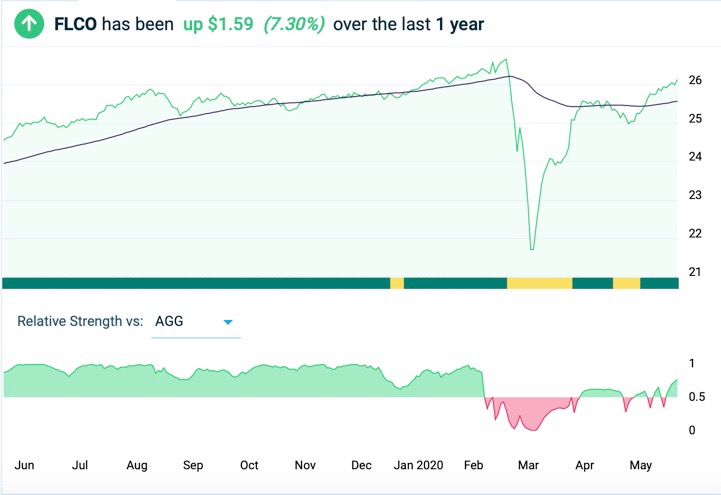

Pimco Enhanced Low Duration Active ETF (LDUR) (ETF Home):

Images from PortfolioWise – Powered by S&P Global Market Intelligence/ClariFi

This is another actively-managed ETF, and if there’s ever a place where active management is needed today, it’s probably so when it comes to the challenge of getting a non-ridiculous yield from a fixed-income portfolio with a very low duration. The SEC Yield reported by LDUR as of 6/8/20 is 2.53% and the effective duration is 2.50 years. It takes a lot to accomplish that including a lot of interest-rate and credit analysis and a willingness to work with derivatives that relate to the fixed-income world. The yield, Power rank, Group rank and risk metrics (Beta of 0.20 and Low Volatility) suggest PIMCO, a firm well-regarded in fixed income, is getting it done here.

If this were a passively-managed portfolio in which everything is held to maturity, investors would likely be locked into noteworthy — but acceptable in the context of the fixed income markets — capital losses as security prices trend from premium levels to face value at maturity bringing the total return down to the extremely low levels we see for other short-term ETFs. But remember; this is an active fund so the managers can trade among different maturities, credits, and security types to avoid a theoretical decline from premium to face value.