The Trump era has so far been a painful time for conservative investors (like me). Success in equities has come to those as bold as the president himself. I won’t comment on how much longer this can serve our Commander in Chief (such prognostication is outside my wheelhouse), but I can and do suggest that in the stock market, it would be a good idea for the the brave to back away a bit from the edge, and be a bit friendlier to who use the Q-word (quality).

The Appetite For Risk Has Been Real

There are many ways to measure risk-taking versus avoidance in the market. My favorite is to compare the performance of the iShares Edge MSCI USA Momentum Factor ETF (MTUM) with the iShares Edge MSCI Minimum Volatility ETF (USMV). Both are model-based portfolios constructed exactly the way the fund names suggest they are constructed. I monitor the relative performances of these ETFs by constructing a simple screen onPortfolio123. The screen has one rule that tells me to buy MTUM. For testing purposes, I compare it to a benchmark that consists of USMV.

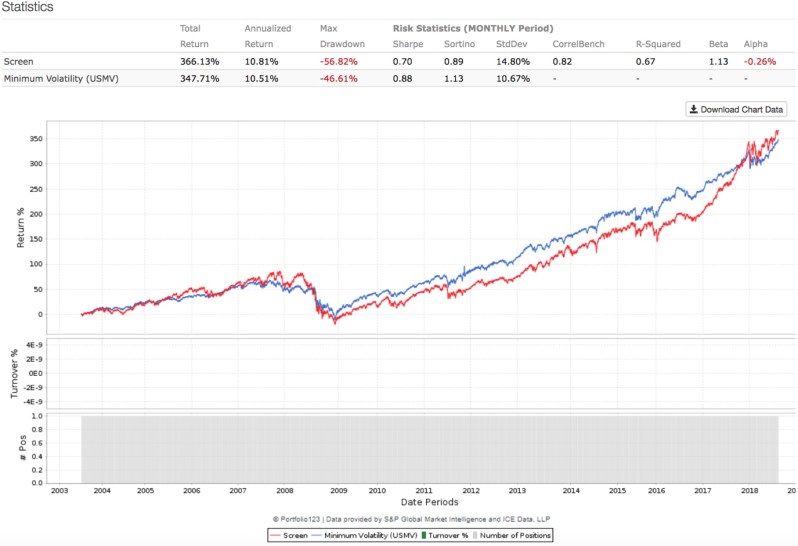

Figure 1, taken from the Portfolio123 screen back-tester, shows how these funds have performed over the past 15 years (Note: The ETFs have existed only since 2013; data before that is pro forma and is based on the indexes the funds are designed to track.)

Figure 1

We see that over the span, momentum (risk taking) has usually not been productive. This is consistent with other research that has depicting stronger than theoretically likely performance of low-risk strategies. (See, e.g., a paper describing Warren Buffett’s alpha and the betting- against beta phenomenon.)

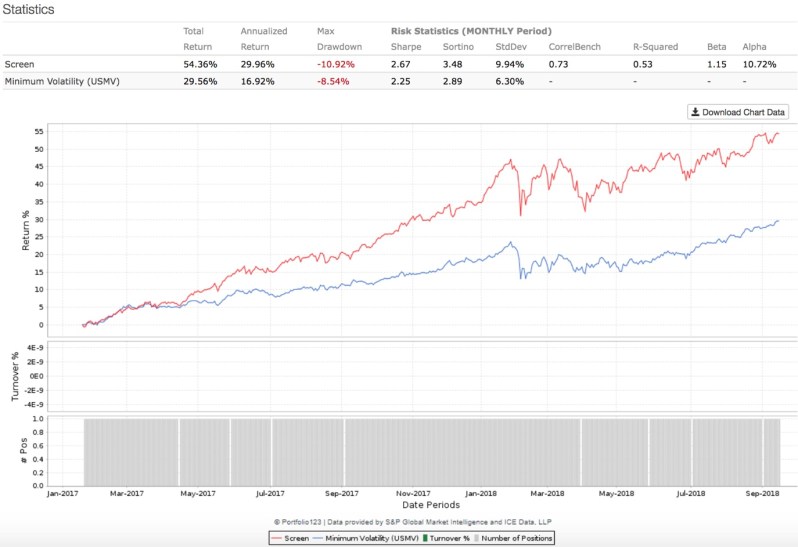

Lately, though, things have been out of whack. There’s much that’s debatable about Donald Trump’s presidency, but two things are absolutely and objectively clear. The stock market has been a powerhouse — SPY returned 18.03% from inauguration day (1/20/17) through 9/14/18 — and risk has beaten the daylights out of prudence: MTUM returned 29.96% versus 16.86% for USMV. See Figure 2.

Figure 2

This is a different aspect of a phenomenon about which I commented in recent posts discussing my Goldilocks Value screens (a large-cap version and a small-cap version). Essentially, we’ve been enjoying great things in terms of the economy and earnings, helped by the mega tax cut, and we continue to power ahead. Risk is a concern when we anticipate tough times, not boom conditions.

Time To Consider A Cold Shower?

Look again at Figure 1, particularly the most recent portion of the graph. Visually, it looks as it MTUM’s strength viz. USMV has started to wane. Table 1, a numeric summary of the 15-year trends, confirms that it’s not an optical illusion. MTUM’s superiority to USMV can no longer be taken for granted.

Table 1

| Measurement Periods | Total Returns (%) | Reward for Risk | ||

| Start | End | MTUM | USMV | MTUM – USMV |

| more risk | less risk | |||

| Latest Period | ||||

| 08/27/18 | 09/17/18 | 1.00% | 1.49% | -0.49% |

| 5/27/18 | 08/26/18 | 6.19% | 8.27% | -2.08% |

| 52-Week Periods | ||||

| 08/28/17 | 08/27/18 | 28.28% | 15.14% | 13.14% |

| 08/29/16 | 08/28/17 | 21.32% | 11.09% | 10.23% |

| 08/31/15 | 08/29/16 | 11.04% | 16.67% | -5.63% |

| 09/02/14 | 08/31/15 | 8.63% | 7.47% | 1.16% |

| 09/03/13 | 09/02/14 | 25.48% | 19.45% | 6.03% |

| 09/04/12 | 09/03/13 | 16.07% | 13.84% | 2.23% |

| 09/06/11 | 09/04/12 | 20.80% | 23.21% | -2.41% |

| 09/07/10 | 09/06/11 | 13.30% | 13.72% | -0.42% |

| 09/08/09 | 09/07/10 | 9.72% | 11.55% | -1.83% |

| 09/08/08 | 09/08/09 | -23.94% | -15.23% | -8.71% |

| 09/10/07 | 09/08/08 | -9.72% | -2.64% | -7.08% |

| 09/11/06 | 09/10/07 | 20.25% | 10.29% | 9.96% |

| 09/12/05 | 09/11/06 | -2.74% | 7.74% | -10.48% |

| 09/13/04 | 09/12/05 | 28.77% | 14.61% | 14.16% |

| 09/17/03 | 09/13/04 | 8.68% | 15.17% | -6.49% |

| Summary of 13-Week Sub-Periods | ||||

| Average | 2.99% | 2.76% | 0.23% | |

| Up Periods | 5.65% | 5.00% | 0.65% | |

| Down Periods | -9.13% | -7.41% | -1.72% | |

Projecting Forward

This is a great example of why we’re always told that past performance cannot assure future outcomes. What past performance would one want to project? The last three-and-a-bit months? The two 12-month periods spanning 8/29/16 through 8/27/18? Or should we assume most of the 13 periods before that constitute the norm?

Statistically speaking, we have to pay homage to the idea of reverting to the mean; a tendency of unusual situations to eventually meander back toward what, based on larger samples, is seen as normal. That alone supports a view that we ought to think about moderating risk. But even beyond reversion to the mean and statistical probability, as good as the headline data continues to be, there are some real-life concerns it’s getting harder to ignore.

- Unless economic activity takes a surprising and meaningful turn for the worse (that, in and of itself, a troublesome albeit not likely at the moment scenario), interest rates are clearly heading upward;

- Just when it seemed Trump may back off from his vintage 1930s tariff war he turns around and decides to escalate with China, thus putting all of the great economic data that has been driving stocks and risk-taking in jeopardy;

- There is upward pressure on wages based simply on supply and demand, and it may be exacerbated by political pushback in response to the way corporations have been using tax-break windfalls to buy back stock.

- Etc.

Actually, I hate worry lists like this. I can’t recall a single day in my career when I couldn’t come up with one just as good if not better. I’ve often said that since humankind invented the wheel and some naysayer whined about how difficult it would be to monetize the thing, it has never been a good time to invest; wars, plagues, natural disasters, empires rising, empires crumbling, mass genocide, revolution, bad harvests, and on and on . . . Yet through it all, ownership of productive assets, despite some nasty zigs and zags here and there, has been good. So even now, I hesitate to turn bearish.

But there’s a big difference between saying “sell stocks” versus saying “hold stocks and even buy more, but consider pulling back a bit on the degree of risk you take.” I’m not saying the former. I am proposing the latter.

A Built-For-Stability Model

On paper, this is an easy strategy to implement. Just invest in stocks with low standard deviation (a measure of share return volatility) and/or low Beta (a measure of share return volatility relative to the movements of the overall market).

If we could be sure that past results are indicative of what the future holds, such a strategy would be perfect and I’d use one that does just that. Unfortunately, the world in which we live is such that not only are we unable to be certain of this, we can be as sure as human experience allows us to be that there will be many instances in which this turns out to not be so,

So rather than bet the farm on statistical report cards that show what has happened in the past, I built a strategy on a foundation constructed with the elements that make a company’s profit stream likely to be more stable than average. I did this by limiting consideration to stocks in a large capitalization universe that rank in the top 35% in terms of the Portfolio123 Basic: Quality ranking system.

Why, one might wonder do we consider the top 35% rather than the best of the best, say the top 5%? Because that would be overkill. I’m not an awards committee (“And now, the prize for best gross margin over the past 12 months goes to . . . “). I’m just an investor working to cope as best I can with an uncertain future, All I need is enough strength in terms of quality to allow me to presume that statistical stability comes from something real, something more likely than not to be capable of manifesting in the future. Demanding too much would likely eliminate many truly worthy stocks.

Having established this important “Quality” gatekeeper, I can now make use of conventional statistical risk measures. But even here, I go the extra mile. To mitigate against the possibility of aberrations getting through (an ever-present risk of any quantitative methodology), I use a collection of risk measures computed over a variety of time periods.

After I first screen based on Quality, I next require that Beta, calculated over various time periods, must be less than 0.90 (1.00 is signifies average volatility relative to the market). The remaining stocks are then sorted under a Stability-oriented ranking system and I select up to the 30 best (most stable) stocks for the portfolio.

Note on valuation: Don’t be surprised if you find stocks here with high valuation ratios. It is a common error to assume low valuation equals low risk. In fact, it’s the opposite. My Strategy Design Cheat Sheet shows why ideal P/E rises as risk falls (i.e., as quality increases). But even without reading that, it make sense. Risk protection anywhere in life is a valuable service for which we expect to pay. That’s why we buy fire insurance, auto insurance, “portfolio insurance” (hedging and associated costs), why we avoid junk bonds, etc. So we should expect lower-risk stock to be priced at a premium.

Performance

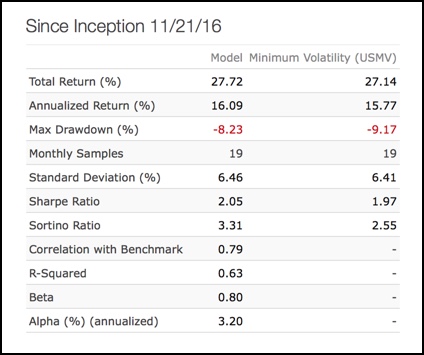

Figure 3 shows that since the model was launched, it has modestly outperformed USMV and when we factor in risk, we see that it has generated a positive alpha relative to the ETF.

Figure 3

The Stocks

Here are the stocks presently in the portfolio.

CONSUMER DISCRETIONARY

- McDonald’s Corp (MCD)

- Starbucks (SBUX)

- TJX Companies (TJX)

CONSUMER STAPLES

- Altria Group (MO)

- Church & Dwight (CHD)

- Clorox Co (CLX)

- Hershey Co (HSY)

- Hormel Foods (HRL)

- Ingredion (INGR)

- Kellogg (K)

- Procter & Gamble Co (PG)

FINANCIALS

- AFLAC (AFL)

- Brown & Brown (BRO)

- CME Group (CME)

- Progressive Corp (PGR)

HEALTH CARE

- Encompass Health (EHC)

- Johnson & Johnson (JNJ)

- Pfizer (PFE)

- Quest Diagnostics (DGX)

INDUSTRIALS

- Verisk Analytics (VRSK)

INFORMATION TECHNOLOGY

- Check Point Software Technologies (CHKP)

- CGI Group (GIB)

- Fiserv (FISV)

- Genpact (G)

- Henry (Jack) & Associates (JKHY)

MATERIALS

- AptarGroup (ATR)

- Ecolab (ECL)

- International Flavors & Fragrances (IFF)

REAL ESTATE

- Public Storage (PSA)

TELECOMMUNICATIONS SERVICE

- Verizon Communications (VZ)

8 thoughts