I struggled in high-school chemistry. No, struggled isn’t the right world. As academically strong as I was in everything else, my inability to comprehend all things periodic table threatened to turn me into what back then was known as a “super senior,” (one who was unable to graduate in four years and had to come back for more). The only way I got through it was to get extra credit by doing clerical work for the teacher, and while alone in the office with a fellow student worker . . . Can that: I take the Fifth. Later, in my decades analyzing stocks, I’d always managed to steer clear of chemical companies fearing I’d lose my lunch if I had to read and think about their businesses. But finally, specialty chemical producer Huntsman (HUN) broke me down. I’m now facing my phobia and writing — favorably no less from an investment point of view —about this sort of company.

Preliminary Note: Why this Stock is Being Considered

It’s important, before you start to read about or evaluate a stock, to know why the it came under consideration and be comfortable soundness of those reasons. Huntsman came to my attention through an EPS Surprise screen I created on Portfolio123 that looks among the constituents of a Russell 3000-like universe for companies that experienced a positive EPS surprise in the latest quarter and which ranked highly under criteria relating to Value and Company Quality. Huntsman was one of the passing stocks that ranked in the top 10 under a general analyst-sentiment ranking system I used for the final sort. Details of the approach are described in a 6/8/18 blog post.

Is My Aversion a Bullish Signal?

There is a lot that put me off as a kid and as a teen that I love now. I actually read War and Peace (all of it — no Cliffnotes) on my own to pass the time riding regularly on the subway and loved it. I get and appreciate Shakespeare now, and classical music, and baroque music (and I now know the difference), and poetry. But my capacity for personal growth is not unlimited. Try as I might, and knowing Huntsman’s screen-based investment potential, I still can’t wrap my arms around the likes of Polyurethanes (polyurethane chemicals, including methyl diphenyl diisocyanate, polyols, thermoplastic polyurethane, propylene oxide, and methyl tertiary-butyl ether products), Performance Products (amines, maleic anhydrides, surfactants, linear alkyl-benzene, ethylene glycol, ethylene oxide, and olefins), Advanced Materials (epoxy, acrylic, and polyurethane-based polymers formulations; high performance thermoset resins and curing agents; and base liquid and solid resins). In case you haven’t guessed, those are three Huntsman business segments. The fourth, Textile Effects, I can actually comprehend (textile chemicals, dyes, and inks).

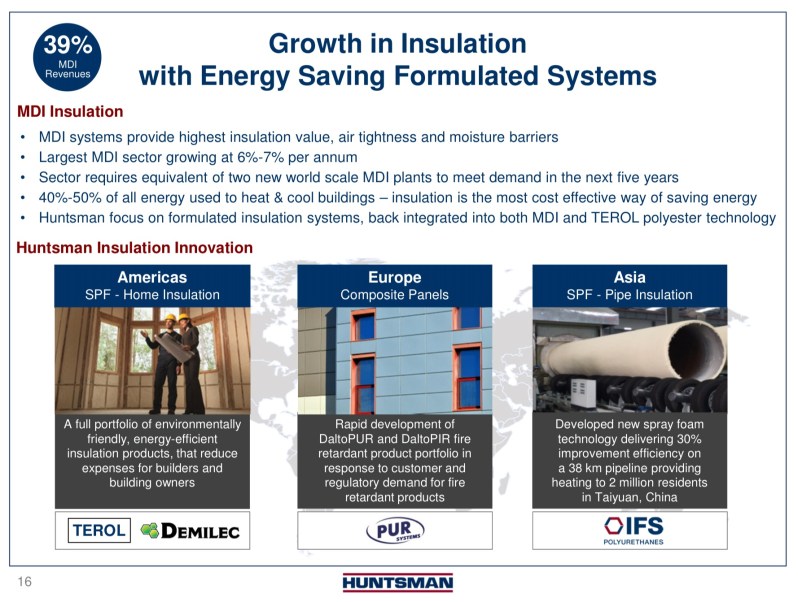

It’s biggest and most important line is methyl diphenyl diisocyanate which, thank God, they abbreviate as MDI. The following two slides from the company’s June 6, 2018 Investor Presentation make it clear that building insulation is the big driver here, but that MDI has other uses elsewhere.

The MDI business is driven by construction and by substitution of MDI for other, less effective, alternatives, particularly in residential construction, where penetration remains low. Aside from this, it’s most practical for investors to treat Huntsman’s overall business as one that is sensitive to trends in overall global economic activity.

The MDI business is driven by construction and by substitution of MDI for other, less effective, alternatives, particularly in residential construction, where penetration remains low. Aside from this, it’s most practical for investors to treat Huntsman’s overall business as one that is sensitive to trends in overall global economic activity.

Ultimately, I thank legendary stock-picker Peter Lynch for giving me the fortitude to stay with this stock. In Chapter 8 of What Works on Wall Street, entitled “The Perfect Stock, What a Deal!” Lynch explains certain characteristics that attract him to a stock. First on the list is a company having a boring, or better, ridiculous, name. Huntsman doesn’t make the grade there: It’s name is neutral. But it is a perfect example of Lynch’s second desirable trait, doing something dull:

“A company that does boring things is almost as good as a company that has a boring name, and both together is terrific. Both together is guaranteed to keep the oxymorons away until finally the good news compels them to buy in, thus sending the stock price even higher. If a company with terrific earnings and a strong balance sheet also does dull things, it gives you a lot of time to purchase the stock at a discount. Then when it becomes trendy and overpriced, you can sell your shares to the trend-followers.”

Kindle Loc. 1969-73.

So is there anything to that, or is it just stale guru folklore? Lynch’s fame comes from his tenure at the helm of the Fidelity Magellan mutual fund in 1977-90. That’s a long time ago; pre internet, pcs with floppy discs. Surely we’re too sophisticated now to allow good companies to slip through just because a company’s business is has all the excitement of a bottle of Ambien, or invokes memories of high-school dread. Let’s see.

Table 1

| HUN | Medians | ||

| Industry | S&P 500 | ||

| PE using Est CurYr EPS | 10.36 | 16.75 | 17.65 |

| PE using Est Next Y EPS | 9.88 | 14.76 | 16.12 |

| PEG Ratio | 1.32 | 1.35 | 1.67 |

| Price/Sales | 0.93 | 1.60 | 2.60 |

| Price/Book | 2.78 | 2.94 | 3.29 |

Maybe not. In fact, maybe the modern era is even more averse to snooze-inducing business profiles. Imagine an analyst contemplating going on CNBC to plug Huntsman and being told, by the producer, it’ll be three minutes; not just to talk about Huntsman but for the entire segment. The analyst won’t decline the segment but will make peace with the reality that nobody will remember anything he or she said about Huntsman (that’s fine; it’s only important that others notice that so-and-so was on TV).

Beyond Value

Reasonable, or even stupendous valuation ratios alone can never justify bullishness on a stock. Value is inextricably intertwined (of my favorite law school phrases) with Growth and Quality. (Seriously — see Appendix A to this this blog post for details on why that’s so.)

Growth is the hardest thing to evaluate. We know all about historic growth but that doesn’t count unless we have good reason to assumer it will persist into the future, and often it doesn’t. We need to invest for tomorrow and as humans, that’s hard to envision. I’ve done a fair amount of work on ways to do this, and lately, I’ve been using analyst-related data (forecasts, surprise, revisions) as a proxy for favorable future growth-related expectations. So that’s covered here by Huntsman’s having passed muster on my Earnings Surprise screen, which included evaluation under a ranking system based on other analyst-related data-points.

Company Quality is another important but often-overlooked element in assessing valuation ratios. High quality, which translates to reduced business risk reduces “required return” and that, all else being equal, increases fair value (again see Appendix A of this blog post).

Quality boils down to returns on capital which depend on the interaction of margin, turnover and finances. Table 2 dishes on this.

Table 2

| HUN | Medians | ||

| Industry | S&P 500 | ||

| % Gross Margin — TTM | 26.22 | 32.52 | 42.23 |

| % Gross Margin — 5Y Avg | 17.55 | 32.03 | 40.20 |

| % Operating Margin — TTM | 11.782 | 11.31 | 17.32 |

| % Operating Margin — 5Y Avg | 8.43 | 10.90 | 17.52 |

| Total Debt to Equity — MRQ | 0.80 | 0.86 | 0.80 |

| LT Debt to Equity — MRQ | 0.79 | 0.79 | 0.71 |

| Interest Coverage TTM | 7.10 | 5.77 | 7.37 |

| Inventory Turnover TTM | 5.27 | 4.68 | 5.40 |

| Asset Turnover TTM | 0.86 | 0.71 | 0.52 |

| % Return on Assets – TTM | 5.50 | 4.93 | 5.17 |

| % Return on Assets – 5Y Avg | 3.70 | 5.21 | 5.35 |

| % Return on Investment – TTM | 11.88 | 8.46 | 9.80 |

| % Return on Investment – 5Y Avg | 8.40 | 9.04 | 9.57 |

| % Return on Equity – TTM | 25.45 | 14.05 | 15.24 |

| % Return on Equity – 5Y Avg | 21.20 | 13.27 | 14.17 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols; ratios based on Portfolio123 protocols. TTM = trailing 12 months MRQ = Most Recent Quarter

High up in the Table, we see that Huntsman is not a margin story per se. Margins have ben better lately, thanks to lower prices of inputs for the company’s petrochemicals, But really, this is about turnover. Is turnover more important than margins? No. Nor are margins more important than turnover. It’s the combination (manifested in returns on assets, investment, and equity) that count.

But here’s where the sizzle-boredom theme comes back. Many in the investment community understand and appreciate margin, but tend to give turnover short shrift, perhaps because the definition of the latter feels less concrete. (Sales divided by Assets, or how many times the asset base turns over in a year; good luck trying to explain that to a novice in 30 seconds or less. The best I can do is say “High volume; they sell many things cheaply instead of a few expensive things”).

Dropping down now to Return on Assets, we see that Huntsman did outperform the industry over the last 12 months, but not so in terms of 5-year average.

Uh oh. Does this suggest the company is on a high right now due favorable costs, but might be prone to reversal if pricing in its materials markets changes?

Return on Assets can be rephrased as Return on Every Darn Thing The Company Has Its Corporate Hands On, no matter how solid or temporary.

If we want to measure return on the more substantial things, the items of permanent capital (equity and long-term debt, the sort that tends to be refinanced rather than repaid), we can do that by stepping down to Return on Investment. Here, we see that the trailing 12 months was above par. But now, we also see that the 5-year average is almost even with the industry median.

We’re not finished. Return on Equity measures profits only against the equity portion of capital. This number can really be boosted if a company is willing to use debt. Put more simplistically, my dollar can go a lot further if I make more use of other people’s money. This is the most complete measure of a firm. It measures the effectiveness of the basic business operation. And it measures the effectiveness of the firm’s philosophy of doing business, the way it finances itself.

In this regard, Huntsman is a clear winner, against both industry and S&P 500 medians, and in both time periods (trailing 12 months and 5-year average).

I may hate reading Huntsman’s business description but I love looking at its ROEs. Then again, I’m sure there are plenty of chemists on Huntsman’s payroll who are really into polyurethanes and stuff like that, but glaze over when confronted with a set of financials. Different strokes for different folks, and you have to love the way the capital markets serve to bridge these differences.

Now, before we get too giddy about the ROEs, we do have to make sure Huntsman isn’t piling on so much debt as to endanger itself. Let’s climb back up Table 2 to the debt ratios and interest coverage. Huntsman definitely has debt, but its not excessive as a portion of capital; actually, it’s noticeably mundane (which is a good thing, I had more than enough debt-induced excitement back when I did junk bonds in the ‘80s). Interest coverage is an area of superiority for Huntsman. (Back in the ‘80s, I’d have killed for a coverage ratio of 1.25-1.5 and 2.0 would have made me faint from excitement.)

Yeah, yeah, good stuff. But how does this help shareholders (besides how it boosts valuation ratios, as we’d all know if we felt like reading the now-three-times plugged Appendix A )?

Table 4 shows another angle. It shows in a more dollars-and-cents manner what’s possible when companies have good fundamentals.

Table 4

| $ mill. | |||||

| The key Inflows: | Important Outflows | Surplus | |||

| Cash Fr. Oper. | Dividend | CapEx | Acquisitions | ||

| 2012 | 774 | 96 | 412 | 18 | 248 |

| 2013 | 708 | 120 | 372 | 66 | 150 |

| 2014 | 760 | 121 | 465 | 960 | -786 |

| 2015 | 575 | 121 | 461 | -4 | -3 |

| 2016 | 1,088 | 120 | 318 | 0 | 650 |

| 2017 | 1,219 | 120 | 282 | 14 | 803 |

| TTM | 1,289 | 129 | 263 | 28 | 869 |

Data from S&P Compustat via Portfolio123.com and reflects Compustat standardization protocols

Yep. It means what it seems to mean. Huntsman is a strong generator of excess cash (more than it needs for reinvestment in its business and payment of dividends). This is why it was able to spend $960 million for acquisitions in 2014 without blowing up its balance sheet. And its why it’ll probably be able to do more cool things down the road.

Acquisitions are not always considered cool by shareholders, but the Street is more accepting when the balance sheet can handle it, and in fact, Huntsman has been very attentive to its debt keeping it in line and paying down to keep it that way. Maybe there will be more share buybacks in the future. Or maybe there will be an improvement in the rate of dividend growth, something the company can afford and which would add spice to the already good (by today’s measly standards) yield.

Table 4

| HUN | Medians | ||

| Industry | S&P 500 | ||

| Dividend Yield % | 1.98 | 1.42 | 1.80 |

| Dividend Growth 5Y % | 4.15 | 6.47 | 9.93 |

| % Payout Ratio — TTM | 23.24 | 31.10 | 40.31 |

| % Payout Ratio — 5Y Avg | 33.11 | 33.11 | 35.68 |

Conclusion

Too bad I hadn’t learned to find and evaluate companies-stocks like Huntsman back in my high school days. I might have been motivated to work harder in chem and pass the $^&@ class with much less angst.